Submarine Power Cable Market Size and Forecast Growth

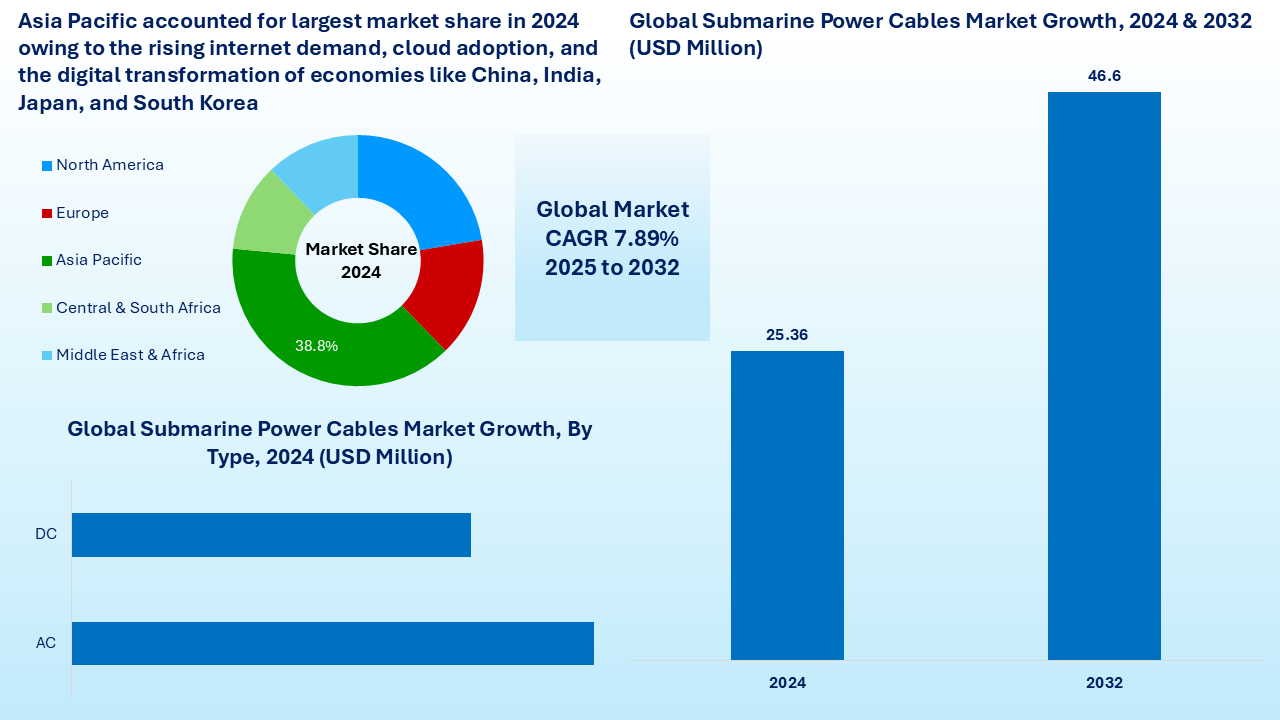

According to Novatrends Market Intelligence, the global submarine cable market size is valued at USD 25.36 billion in 2024. The Submarine power cable market is poised for significant growth, projected to expand significantly with CAGR 7.89% from 2025 to 2032. The submarine power cable market is experiencing robust growth driven by the surging demand for high-speed internet, expanding global data traffic, and increasing investments in intercontinental communication infrastructure. These undersea cables, which carry over 95% of international data, are critical for supporting global connectivity, cloud services, and international business operations. Rising investments in offshore wind projects, advancements in high-voltage transmission technology, and the need for inter-country grid connectivity are some of the major factors acting as market drivers for submarine cables.

Key stakeholders—including telecom operators, cloud service providers, and governments—are heavily investing in new cable routes and advanced fiber optic technologies to enhance bandwidth capacity and network resilience. The market is further propelled by rising 5G deployment, data center interconnectivity, and strategic initiatives to bridge digital divides across developing regions.

Industry Snapshot

Market Driver: Rising Demand for Data Transmission Networks to drive Market Growth

The submarine power cable market is being significantly driven by the exponential rise in global internet usage, cloud service adoption, and digital data consumption. With over 95% of international data traffic carried through undersea cables, the demand for reliable, high-capacity communication infrastructure has intensified. The surge in video streaming, telecommunication services, online gaming, and remote work culture has elevated the need for robust data transmission networks. Cloud providers like Amazon Web Services, Google, and Microsoft are increasingly investing in private submarine cable projects to ensure low-latency, high-speed connectivity between their global data centers.

Furthermore, the widespread rollout of 5G and the growing Internet of Things (IoT) ecosystem necessitate enhanced bandwidth and resilient backhaul networks. Governments and private entities across Asia-Pacific, Africa, and Latin America are also investing in subsea infrastructure to bridge the digital divide and support economic development. Advancements in fiber optic technology, including wavelength division multiplexing (WDM) and space division multiplexing (SDM), are allowing for higher data throughput and more efficient cable utilization. Overall, the convergence of digital transformation, technological innovation, and escalating data demands is propelling strong growth in the global submarine power cable market.

Market Restraint: High Capital Investment to Restraint Market Growth

Despite its promising trajectory, the submarine power cable market faces several critical restraints. High capital expenditure remains a significant challenge, as building and deploying a single submarine cable system can cost hundreds of billions of dollars, limiting participation to large telecom and technology players. The process of cable deployment involves lengthy planning, permitting, and regulatory approvals across multiple jurisdictions, which can cause delays and escalate costs.

Additionally, subsea cables are vulnerable to physical damage from natural disasters such as undersea earthquakes, as well as human activities like fishing, anchoring, and dredging, which can disrupt services and incur expensive repair operations. Cybersecurity is also a growing concern, with the potential for cable tapping or sabotage posing risks to sensitive international data and national security. Environmental concerns around marine ecosystems and the difficulty in navigating maritime laws further complicate cable installation in ecologically sensitive zones. Moreover, geopolitical tensions between nations, particularly in contested waters like the South China Sea, can lead to diplomatic conflicts or blocking of strategic cable routes. These challenges underscore the need for advanced risk management, cross-border regulatory harmonization, and robust cybersecurity protocols to ensure the continued growth of the submarine cable market.

Market Opportunity: Rapid Hyper-connectivity and Digital Globalization to Create Lucrative Opportunities

The submarine power cable market holds significant opportunities as the world moves toward hyper-connectivity and digital globalization. One of the most promising areas is the expansion of digital infrastructure in underserved and developing regions such as Africa, Latin America, and parts of Southeast Asia. Governments and international organizations are collaborating with private firms to build regional submarine cable networks that improve access to broadband and cloud services, fueling economic growth and inclusion. Another strong opportunity lies in the rise of hyperscale data centers and increasing enterprise adoption of cloud computing, which are creating demand for dedicated, high-speed international connections. Innovations like SDM (Space Division Multiplexing), AI-driven cable monitoring, and improved fault localization systems are opening new doors for efficiency and scalability in network operations.

Additionally, the integration of submarine cables with offshore renewable energy projects, such as wind farms, offers dual utility—power transmission and data communication—creating new investment models. Strategic collaborations between telecom carriers, OTT players, and infrastructure providers are expected to yield cost-sharing and technological innovation. As global data sovereignty becomes more critical, nations may also push for domestic landing stations and secure routes, fostering regional opportunities for infrastructure development. Overall, these factors signal long-term, sustainable growth potential for the market.

Segmental Overview

By Type

Based on Type, the market is segmented into Direct Current (DC) and Alternating Current (AC) cables. Direct Current (DC) submarine cables are expected to dominate the market, especially in long-distance and high-capacity transmission applications. High Voltage Direct Current (HVDC) cables are more efficient for transmitting electricity over vast undersea distances because they experience lower energy losses compared to Alternating Current (AC) cables. DC systems are preferred for intercontinental interconnections, offshore wind farms, and cross-border power grid integration, where transmission distances often exceed several hundred kilometers.

While AC submarine cables are still used in short-distance applications, such as inter-island or nearshore connections, they become less efficient as distance increases due to capacitive charging currents and energy loss. As a result, the growing demand for high-voltage, long-haul underwater power and data transmission—driven by renewable energy integration, inter-country power connections, and large-scale subsea infrastructure projects—is expected to keep DC cables at the forefront of the market.

By Core Type

Based on Core Type, the market is segmented into Single Core, Multi-Core. Single Core submarine cables are expected to dominate the market due to their widespread use in both telecommunications and power transmission applications. In high-voltage power transmission—particularly in HVDC systems—single core cables are preferred because they offer greater efficiency, easier thermal management, and simpler installation over long distances. Each single core cable typically carries one conductor, and multiple single-core cables are often laid together for three-phase systems or redundancy.

In the telecommunications segment, single core (single fiber pair or multiple fiber pairs in a single sheath) is also widely deployed due to flexibility in network design, modular scalability, and ease of repair or replacement. While multi-core cables are gaining attention—especially in high-density optical fiber applications—they are still emerging and currently used in niche or advanced infrastructure projects.

Multi-core cables offer the benefit of increased data transmission capacity in a smaller footprint, making them attractive for future scaling, particularly in dense urban or data center interconnect applications. However, due to higher manufacturing complexity and costs, their adoption remains limited compared to the established single-core alternatives.

By Insulation Type

Based on Insulation Type, the market is segmented into Single Core, Multi-Core. Cross-Linked Polyethylene (XLPE) is expected to dominate the submarine power cable market by insulation type, owing to its superior thermal performance, higher dielectric strength, and longer lifespan. XLPE insulation is widely used in high-voltage power transmission, particularly in HVDC and HVAC submarine power cables, due to its ability to withstand high temperatures and electrical stress over long durations. It also offers advantages in terms of lower capacitance, which reduces charging currents and makes it highly efficient for long-distance subsea applications.

On the other hand, Ethylene Propylene Rubber (EPR) is typically used in medium-voltage and flexible cable applications, such as dynamic cables for offshore platforms and short-distance connections. While EPR offers excellent flexibility, water resistance, and mechanical strength, it is generally less suitable for high-voltage, long-distance power transmission compared to XLPE.

The growing deployment of offshore wind farms, intercontinental HVDC projects, and grid interconnections has fueled demand for XLPE-insulated submarine cables, solidifying its position as the preferred insulation material in the global market.

By Voltage

Based on Voltage, the market is segmented into Up to 66 KV, 66 KV-220 KV, and Above 220 KV. Submarine cables in the voltage range of 66 kV–220 kV are expected to dominate the global market, primarily due to their extensive use in offshore wind farm connections, inter-island links, and medium-to-long distance power transmission projects. This voltage segment offers an optimal balance between power capacity, transmission efficiency, and cost-effectiveness, making it the preferred choice for a wide range of utility-scale and commercial applications.

While “Up to 66 kV” cables are typically used in short-distance or low-capacity connections, such as nearshore interconnects and smaller renewable projects, their market share remains relatively limited in large-scale infrastructure developments. On the other end, “Above 220 kV” submarine cables, especially those used in High Voltage Direct Current (HVDC) systems, are critical for ultra-long-haul and intercontinental connections. However, their deployment is more capital-intensive, project-specific, and currently confined to a smaller number of high-budget international projects. As offshore wind capacity scales up and grid interconnectivity expands across regions, the 66 kV–220 kV segment is anticipated to witness the highest demand over the next decade.

By Conductor Material

Based on Conductor Material, the market is segmented into Copper, Aluminum. Copper submarine cables is expected to dominate the submarine power cable market by conductor material due to its superior electrical conductivity, higher tensile strength, and reliability in harsh underwater environments. Copper’s ability to efficiently transmit electricity with minimal resistance makes it the preferred choice for both power and communication submarine cables, especially in long-distance and high-capacity applications.

Copper conductors are particularly advantageous in High Voltage Direct Current (HVDC) and subsea telecommunications systems, where consistent performance, durability, and low power losses are critical. Additionally, copper's resistance to corrosion and mechanical stress enhances its suitability for deployment in challenging marine conditions.

Although aluminum is lighter and more cost-effective, it has lower conductivity compared to copper, which can result in higher transmission losses. Aluminum submarine cable is generally used in shorter or cost-sensitive projects, and often requires a larger cross-sectional area to match copper's performance, which increases cable size and complexity. Due to the technical superiority and long-term reliability required in subsea environments, copper remains the dominant material in most commercial submarine cable installations.

By End-Use

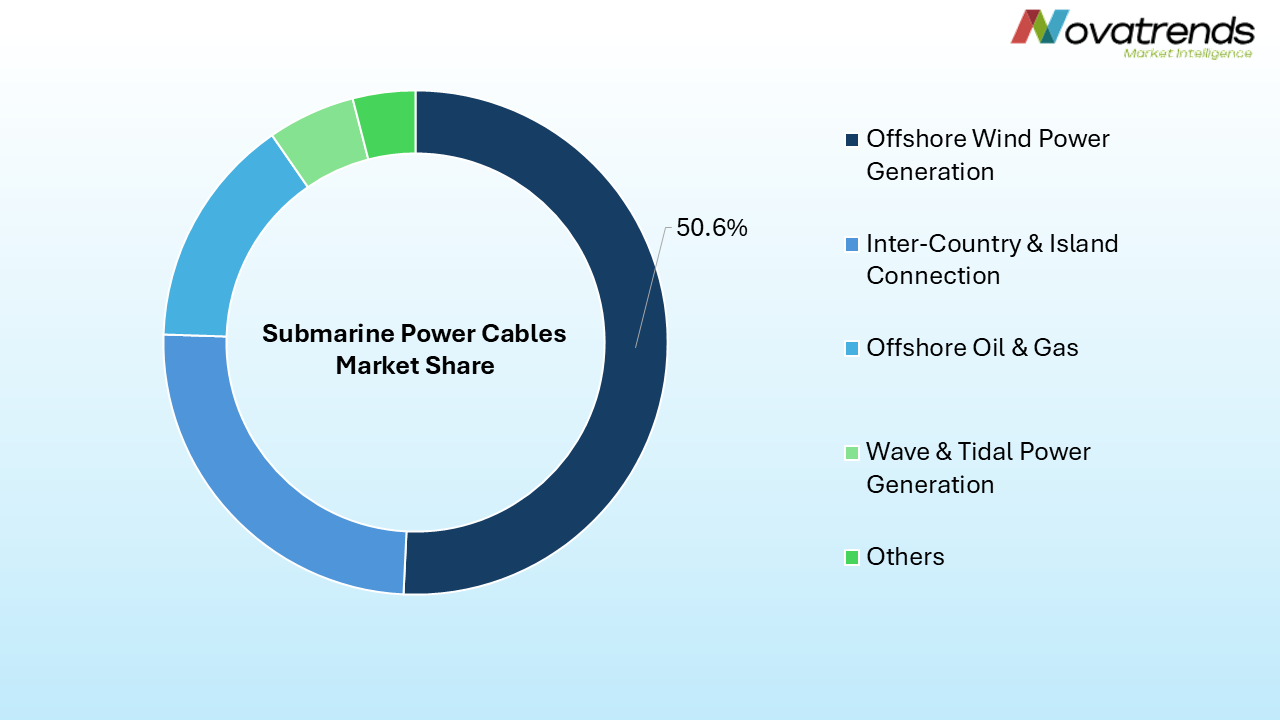

Based on End-Use, the market is segmented into Offshore Wind Power Generation, Offshore Oil & Gas, Island Connection, Wave & Tidal Power Generation. Offshore Wind Power Generation is expected to dominate the submarine power cable market by end-use, driven by the global transition toward renewable energy, increasing investments in offshore wind farms, and aggressive government targets for carbon neutrality. As offshore wind projects move farther from the coast into deeper waters, the demand for high-capacity, long-distance submarine power cables continues to rise.

These projects rely heavily on High Voltage Alternating Current (HVAC) and High Voltage Direct Current HVDC submarine cables to transmit electricity generated by wind turbines to onshore grids. The rising number of large-scale offshore wind farms in Europe, Asia-Pacific (notably China and South Korea), and North America has positioned this segment as the key growth driver. While Offshore Oil and Gas has traditionally been a significant end-user of submarine cables—mainly for power supply and communication between offshore platforms and onshore facilities—it is witnessing relatively slower growth due to the global energy shift away from fossil fuels. Island connections and Wave & Tidal Power Generation represent smaller but emerging segments, with demand primarily driven by energy access for remote regions and pilot-scale renewable energy projects.

Regional Overview

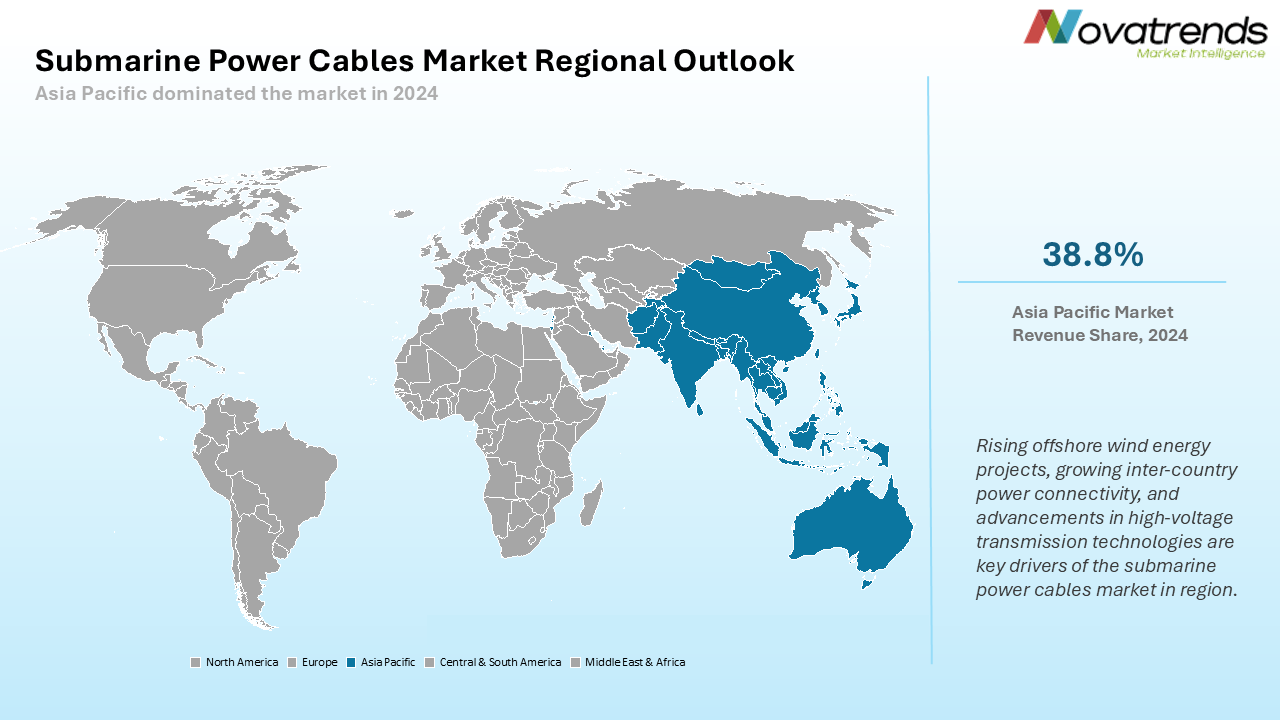

The submarine power cable market is expanding globally, with North America leading through investments by tech giants in transoceanic connectivity. Europe remains a key hub due to its mature infrastructure and leadership in offshore wind submarine cables. Asia Pacific is the fastest-growing region, driven by high internet demand, data center expansion, and regional interconnectivity. Central and South America are improving connectivity through strategic projects linking with Europe and North America. Meanwhile, the Middle East & Africa are emerging as vital transit routes and growth markets, with increasing infrastructure investments aimed at bridging the digital divide and enhancing global data flow.

North America

North America submarine cable industry is led by the United States and Canada, driven by rising demand for hyperscale data centers, cloud connectivity, and digital transformation. U.S.-based tech giants like Google, Microsoft, and Meta are heavily investing in private submarine cable projects to connect North America with Europe, Latin America, and Asia. The region also sees increasing focus on latency reduction and secure data transmission, making transatlantic and transpacific routes critical. Regulatory support, strong infrastructure, and technological advancement continue to position North America as a global hub for subsea connectivity and capacity expansion.

Europe

Europe submarine power cable market is expected to grow at significant rate due to its mature infrastructure, high internet penetration, and leadership in offshore wind energy deployment. Countries such as the UK, Germany, Norway, and France serve as key landing points and connectivity gateways to North America, Africa, and Asia. The region is a pioneer in sustainable energy, using submarine cables to connect offshore wind farms to mainland grids. Additionally, European Union policies support cross-border digital infrastructure, making the region a critical corridor for data and power transmission. Investment in both telecom and energy subsea networks ensures Europe's continued dominance and innovation in this sector.

Asia Pacific

Asia-Pacific submarine cable market is the fastest-growing region in the global market, fueled by rising internet demand, cloud adoption, and the digital transformation of economies like China, India, Japan, and South Korea. The region is a key corridor for intra-Asia and Asia-to-global cable routes, hosting major data hubs and extensive submarine cable landing stations. China’s Belt and Road Initiative includes digital infrastructure expansion, while Japan and Singapore serve as critical gateways for regional and intercontinental traffic. Rapid deployment of offshore wind farms and rising inter-island connectivity needs across Southeast Asia further enhance the market’s momentum in this dynamic region.

Central & South America

Central and South America are witnessing growing investment in submarine cable systems to improve digital connectivity and bridge infrastructure gaps. Countries like Brazil, Chile, and Colombia are key players, offering strategic landing points for transatlantic and transpacific cable routes. The region’s growing tech adoption, data center expansion, and participation in international digital networks are boosting demand. Several projects, such as the EllaLink cable connecting Brazil to Portugal, are enhancing intercontinental data exchange. However, regulatory submarine cable challenges and limited local manufacturing capacity still pose hurdles, though ongoing investments from global tech firms are expected to uplift regional subsea infrastructure significantly.

Middle East & Africa

The Middle East & Africa region is emerging as a critical strategic zone for the submarine power cable market, connecting Europe, Asia, and Africa via key maritime chokepoints like the Red Sea and the Suez Canal. Countries like the UAE, Saudi Arabia, Egypt, and South Africa are leading investments in digital infrastructure and subsea cable landing stations. Africa, in particular, is seeing a surge in projects aimed at improving broadband penetration and closing the digital divide, such as Google's Equiano and Meta's 2Africa cables. Despite infrastructure gaps, the region holds massive potential as a transit and growth hub for global connectivity.

Competitive Landscape

The competitive landscape of the submarine power cable market is characterized by the presence of established telecom operators, cable manufacturers, and tech giants driving global connectivity initiatives. Key players include NEC Corporation, Prysmian Group, Nexans, SubCom LLC, and Hengtong Marine Cable Systems, among others. Additionally, major cloud service providers like Google, Meta, Microsoft, and Amazon Web Services are investing in private submarine cable networks to enhance bandwidth and reduce latency across regions. Strategic collaborations, consortium-based deployments, and technological innovations such as SDM (Space Division Multiplexing) are intensifying competition. Market players are also expanding capacity to meet rising global data transmission demands.

Major Industry Updates

The submarine power cable market is witnessing rapid developments driven by rising AI-powered data demand, growing hyperscale cloud infrastructure, and heightened geopolitical awareness. Major tech companies like Google, Meta, and Microsoft are accelerating the deployment of large-scale subsea networks, including trans-Pacific and intercontinental projects. Security concerns have intensified, with increasing reports of cable sabotage risks prompting governments to enhance maritime surveillance and protection frameworks. Additionally, emerging markets such as Latin America and Africa are becoming key strategic hubs with new cable routes planned to improve regional connectivity. Overall, the industry is evolving with a strong focus on resilience, capacity, and global reach.

- In June 2025, Telecom Egypt, PCCW Global, Sparkle, and Zain Omantel International have signed a memorandum to build the new AAE‑2 submarine cable, linking Hong Kong and Singapore with Italy via Thailand, the Arabian Peninsula, and Egypt. This integrated subsea and terrestrial route will enhance connectivity between Asia, Africa, and Europe, offering higher capacity, lower latency, and supporting growing cloud demand across the regions.

- In May 2025, Prysmian has inaugurated its state‑of‑the‑art plant expansion in Pikkala, Finland, highlighted by a 185‑meter “Prysmian Tower” for high‑voltage submarine cable production, delivering around 1 km of cable daily. Simultaneously, the newly christened cable‑laying vessel Monna Lisa is fully operational — equipped with dual 7,000 t and 10,000 t carousels, hybrid power systems, and deep‑sea laying capability — boosting global subsea infrastructure response and deployment efficiency.

- In March 2025, LS Cable & System is expanding its offshore wind power business via four subsidiaries—Gaon Cable, LS Eco Energy, LS Materials, and LS Marine Solution—which will extend into investment, technology, operations, subsea cable production, core components, vessel support, and maintenance. Leveraging its unique Korean HVDC submarine network expertise, the company aims to fortify its position across the full offshore wind value chain in response to national policy and market trends.

- In February 2025, Meta (formerly Facebook) announced plans Project Waterworth, a 31,000-mile (≈50,000 km) undersea cable system linking the U.S., Brazil, South Africa, India, and Australia. Intended as the world’s longest subsea cable, it will feature 24 fiber pairs and deep-sea burial techniques to ensure durability. The initiative reflects a shift, with big tech—not just telecoms—driving global internet infrastructure deployment.

- In January 2025, Ooredoo Group, in partnership with Alcatel Submarine Networks, is constructing the Fibre in Gulf (FIG) submarine cable to connect Qatar, Oman, UAE, Bahrain, Saudi Arabia, Kuwait, and Iraq. This high-capacity loop features 24 fiber pairs and can deliver up to 720 Tbps, providing secure, low-latency connectivity across the GCC and to Europe. Service launch is slated for Q4 2027, bolstering digital infrastructure for hyperscalers, AI, cloud, and telecom sectors.

- In December 2024, ABB partnered with NKT to electrify and expand NKT’s submarine high-voltage cable factory in Karlskrona, Sweden, by installing a third 200-meter extrusion tower. ABB’s turnkey solution includes UniGear ZS1 switchgear panels and renewable-energy grid connections to support around-the-clock production. This upgraded facility will produce cables for up to 640 kV DC, enabling connection of approximately ten offshore wind farms (~20 GW total capacity), powering 15–20 billion homes annually.

- In May 2024, TenneT begun producing ultra-high-voltage 525 kV cables at LS Cable’s Donghae (South Korea) facility, designed to transmit up to 2 GW of direct current for offshore wind grid connections. These cables, part of a four-system framework, will support the BalWin4 and LanWin1 projects, covering ~1,650 km of cable, with production through 2028 and offshore installation starting mid‑

Key Market Players

- Alcatel Submarine Networks

- SubCom, LLC

- NEC Corporation

- NEXANS

- Prysmian Group

- Hengtong Group

- ZTT

- NKT A/S

- LS Cable & System Ltd

- Sumitomo Electric Industries

- Corning Incorporated

- Hellenic Cables

- Fujitsu Ltd

- Global Marine Group

- HMN Technologies Co., Ltd.

Global Submarine Power Cable Market Research Report- Scope (Customizable)

Scope |

Description |

|

Historic Period |

2018-2023 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Market Revenue |

USD Billion |

|

Market by Type |

AC and DC |

|

Market by Core Type |

Single Core and Multi-Core |

|

Market by Insulation Type |

Cross-Linked Polyethylene (XLPE), Ethylene Propylene Rubber (EPR) |

|

By Voltage |

Up to 66 KV, 66 KV-220 KV, Above 220 KV |

|

By Conductor Material |

Copper and Aluminum |

|

By End-Use |

Offshore Wind Power Generation, Offshore Oil & Gas, Island Connection, Wave & Tidal Power Generation |

|

Market By Region |

North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

|

Countries Covered |

U.S., Canada, Mexico; Germany, France, UK, Russia, Italy, Spain, and Netherlands; China, India, Japan, South Korea, and Australia; Brazil, Argentina; Saudi Arabia, Turkey, Egypt, and South Africa |

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?