Market Overview

According to Novatrends Market Intelligence, the Global Silicon Carbide Market was valued at USD 5.8 billion in 2025 and is anticipated to propel at a growth rate of 14.2% from 2026-2036.

The global silicon carbide market spans two distinct product ecosystems: the high-volume commodity segment of silicon carbide abrasive products, silicon carbide refractory materials, and silicon carbide metallurgical grade; and the high-value specialty segment of silicon carbide semiconductor wafers and silicon carbide power electronics. Silicon carbide for EV applications in traction inverters is the single fastest-growing demand driver — SiC MOSFETs operating at higher voltages, frequencies, and temperatures than silicon equivalents are enabling longer EV range and faster charging. Silicon carbide semiconductor wafers supply semiconductor device manufacturers fabricating silicon carbide power electronics for industrial motor drives, solar inverters, EV chargers, and grid infrastructure. Black silicon carbide abrasives and green silicon carbide products remain large-volume abrasive markets serving silicon carbide grinding wheels, polishing, blasting, and silicon carbide wire sawing for solar wafer production. Silicon carbide ceramic components, silicon carbide heat exchangers, silicon carbide nozzles and liners, silicon carbide crucibles, and silicon carbide mechanical seals serve demanding high-temperature industrial process applications exploiting silicon carbide thermal conductivity.

Market Dynamics

The market is driven by the electric vehicle revolution creating exponential growth in silicon carbide for EV applications, renewable energy expansion requiring silicon carbide power electronics for solar and wind power conversion, and industrial energy efficiency programs adopting SiC motor drives. Silicon carbide sintering technology advances are lowering costs for silicon carbide ceramic components and enabling silicon carbide foam filters for molten metal filtration and silicon carbide coating applications for wear protection. Silicon carbide particle size distribution control is critical for black silicon carbide abrasives and green silicon carbide products performance in precision grinding and lapping. Silicon carbide semiconductor wafers are moving to 150mm and 200mm wafer diameters to reduce cost per device through silicon carbide sintering technology and epitaxial growth improvements. In January 2024, Wolfspeed Inc. opened its Mohawk Valley fab — the world's largest 200mm silicon carbide semiconductor wafers facility targeting silicon carbide for EV applications supply chain scale-up. STMicroelectronics, Infineon Technologies, and ROHM Semiconductor are all expanding silicon carbide power electronics capacity to serve automotive OEM long-term supply agreements for silicon carbide for EV applications.

Segment Analysis

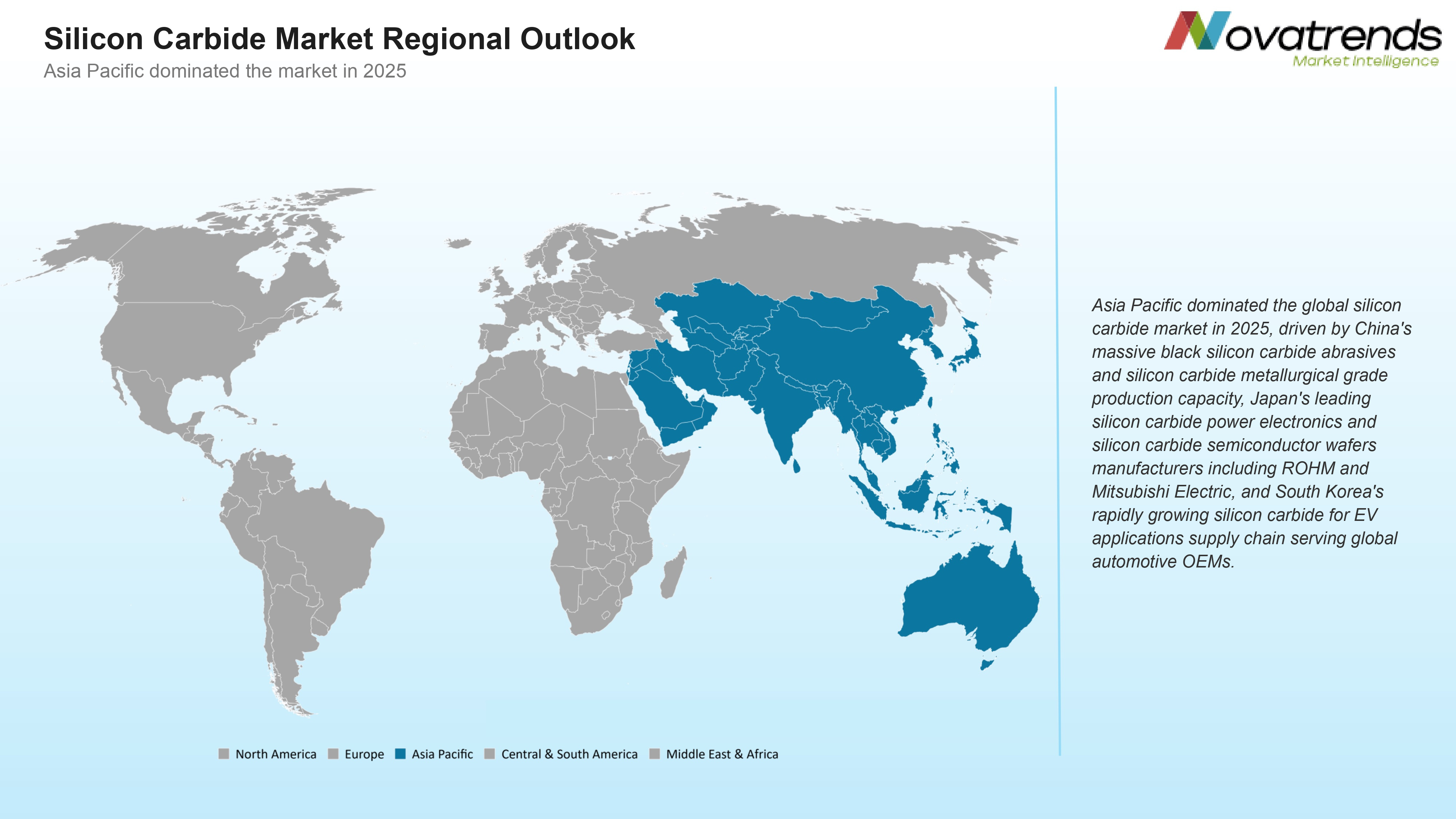

By Grade: Metallurgical Grade holds the largest share of the Silicon Carbide market, supported by strong adoption and well-established supply chains across key end-use industries. Refractory Grade is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Product Type: Black Silicon Carbide holds the largest share of the Silicon Carbide market, supported by strong adoption and well-established supply chains across key end-use industries. Green Silicon Carbide is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Application: Abrasives holds the largest share of the Silicon Carbide market, supported by strong adoption and well-established supply chains across key end-use industries. Semiconductors is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By End-Use Industry: Semiconductor holds the largest share of the Silicon Carbide market, supported by strong adoption and well-established supply chains across key end-use industries. Automotive is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

Recent Developments in Silicon Carbide Market

- In January 2024, Wolfspeed Inc. opened its Mohawk Valley, New York 200mm silicon carbide semiconductor wafers facility — the world's largest — with 2 million SiC device capacity targeting silicon carbide for EV applications and silicon carbide power electronics for automotive and industrial customers globally.

- In April 2024, STMicroelectronics expanded silicon carbide power electronics and silicon carbide for EV applications production capacity under long-term supply agreements with Renault and Volkswagen, advancing silicon carbide sintering technology and silicon carbide semiconductor wafers supply chain localization in Europe.

- In July 2024, Infineon Technologies launched next-generation silicon carbide power electronics devices for EV traction inverters and silicon carbide for EV applications onboard chargers, featuring improved silicon carbide thermal conductivity and silicon carbide coating applications for device packaging thermal management.

- In September 2024, ROHM Semiconductor expanded silicon carbide semiconductor wafers production at its Japan facility, launching silicon carbide mechanical seals and silicon carbide ceramic components for industrial customers alongside silicon carbide for EV applications power module supply to Japanese and European automotive OEMs.

- In December 2024, Saint-Gobain expanded silicon carbide refractory materials and silicon carbide foam filters for steel and aluminum industry molten metal processing, alongside silicon carbide heat exchangers and silicon carbide nozzles and liners for chemical processing industries requiring silicon carbide thermal conductivity performance.

- In March 2025, Fiven (previously Saint-Gobain Ceramics) expanded black silicon carbide abrasives and green silicon carbide products production in Norway, targeting silicon carbide grinding wheels, silicon carbide wire sawing for PV wafer cutting, and silicon carbide particle size distribution quality programs for precision abrasive and polishing applications.

Top Silicon Carbide Market - Key Market Players

- Wolfspeed Inc. (Cree)

- STMicroelectronics

- Infineon Technologies

- ROHM Semiconductor

- Saint-Gobain

- Fiven

- ON Semiconductor (onsemi)

- Robert Bosch GmbH

- II-VI Incorporated (Coherent)

- SiCrystal GmbH (ROHM)

- Denso Corporation

- Mitsubishi Electric Corporation

- GE Aviation (SiC)

- Dow Chemical (Silicon Carbide)

- Washington Mills

Global Silicon Carbide Market Report- Scope (Customizable)

Scope | Description |

Historic Period | 2021-2024 |

Base Year (Esti.) | 2025 |

Forecast Period (F) | 2026-2036 |

Market Values | USD Billion |

By Grade | Metallurgical Grade, Refractory Grade, Semiconductor Grade |

By Product Type | Black Silicon Carbide, Green Silicon Carbide, SiC Semiconductor Wafers, SiC Ceramics |

By Application | Abrasives, Semiconductors, Refractories, Power Electronics, Automotive |

By End-Use Industry | Semiconductor, Automotive, Steel, Renewable Energy, Electronics |

Market by Region | North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

Countries Covered | U.S., Canada, and Mexico; Germany, France, UK, Russia, Italy, Spain, and Netherlands; China, India, Japan, South Korea, and Australia; Brazil, Argentina; Saudi Arabia, UAE, Turkey, Egypt, and South Africa |

Detailed Market Segmentation

- By Grade (Revenue in USD Million)

- Metallurgical Grade

- Refractory Grade

- Semiconductor Grade

- By Product Type (Revenue in USD Million)

- Black Silicon Carbide

- Green Silicon Carbide

- SiC Semiconductor Wafers

- SiC Ceramics

- By Application (Revenue in USD Million)

- Abrasives

- Semiconductors

- Refractories

- Power Electronics

- Automotive

- By End-Use Industry (Revenue in USD Million)

- Semiconductor

- Automotive

- Steel

- Renewable Energy

- Electronics

- By Region (Revenue in USD Million)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Russia

- Italy

- Spain

- Netherlands

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Central & South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Egypt

- South Africa

- North America

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?