Report Overview

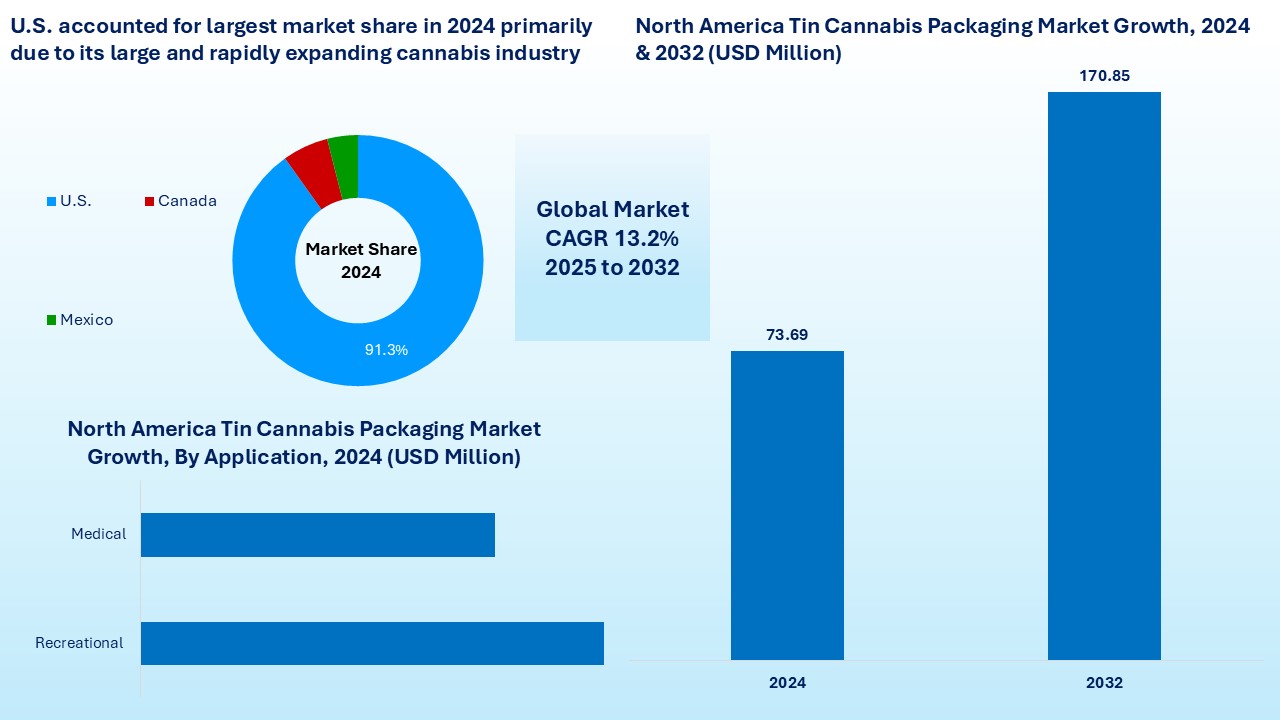

According to Novatrends Market Intelligence, the North America Tin Cannabis Packaging Market is valued at USD 73.69 million in 2024 and is expected to grow at CAGR of 13.2% from 2025 to 2032. The North America tin cannabis packaging market is experiencing steady growth, driven by evolving legalization trends, increasing consumer awareness, and rising demand for sustainable packaging solutions. With the gradual expansion of cannabis legalization across several U.S. states and the established recreational market in Canada, the cannabis industry continues to expand, leading to heightened demand for innovative, compliant, and brand-friendly packaging formats. Tin packaging has emerged as a preferred choice for cannabis products such as pre-rolls, edibles, and concentrates due to its durability, reusability, and premium appeal.

Furthermore, as the cannabis market moves toward sustainability, environmentally conscious consumers are showing preference for packaging that can be recycled or reused. Tin packaging aligns with this shift, as it is more environmentally friendly compared to single-use plastics. The shift in consumer behavior, paired with increasing investment in sustainable packaging innovation, is expected to reinforce the position of tin containers as a leading packaging format.

Industry Snapshot

Market Driver: Legalization, Premiumization, and Sustainability Fuel Demand

The growth of tin cannabis packaging in North America is primarily driven by expanding legalization, rising brand competition, and increasing consumer demand for sustainable and premium packaging formats. As more U.S. states legalize cannabis for medical and recreational use and Canada continues its national-level operations, producers are under pressure to comply with strict packaging standards—especially those involving child resistance and tamper evidence. Tin containers naturally fulfill these needs due to their rigid structure and customizable features, enabling both safety and brand expression.

Furthermore, consumers are becoming more eco-conscious, preferring packaging that is recyclable and reusable. Tin's infinite recyclability makes it an attractive alternative to plastic and glass, aligning with broader environmental goals. At the same time, premiumization is transforming the cannabis space into a lifestyle category, where packaging must be visually distinct and feel luxurious. Brands are leveraging tins for embossed designs, matte finishes, and creative formats that enhance shelf appeal and improve product preservation by shielding contents from moisture and light. As marketing strategies shift toward experiential packaging and tactile differentiation, tin packaging is being seen not just as a container, but as a key part of product identity and customer engagement. These intersecting trends—legal compliance, environmental consciousness, and branding sophistication—are collectively accelerating the adoption of tin packaging across a broad range of cannabis product categories in North America.

Market Restraint: High Costs and Regulatory Complexity Limit Scalability

Despite its functional and aesthetic advantages, tin cannabis packaging faces several barriers that constrain its market penetration. One of the most significant is cost—tin containers are inherently more expensive to manufacture and decorate than flexible or paper-based alternatives, which creates a financial hurdle for small and mid-sized cannabis companies. Custom molds, embossing, and lithographic printing all add to production complexity and require higher minimum order quantities. In addition, tin’s inflexible shape makes it unsuitable for certain product types like loose flower or large-volume edibles that benefit from more pliable containers.

Regulatory fragmentation poses another restraint: each U.S. state and Canadian province enforces unique packaging requirements, making it difficult to create standardized tin solutions without resorting to costly, region-specific SKUs. These regulatory inconsistencies increase time-to-market and force brands to allocate more resources to compliance and redesign. Another overlooked challenge is sustainability perception—while tin is technically recyclable, not all municipalities in North America have strong metal recycling programs. This can lead consumers to view tin less favorably than paper or bio-degradable alternatives, even when tins are objectively more durable and reusable. The combined effect of high production costs, regulatory variability, limited structural flexibility, and uneven recycling infrastructure restricts tin’s broader adoption, relegating it primarily to high-end or niche product categories unless significant cost and infrastructure improvements are made.

Market Opportunity: Innovation and Smart Packaging Can Unlock Growth

Amid regulatory and cost challenges, the North America tin cannabis packaging market still offers ample opportunities for growth through innovation, consumer engagement, and sustainability. Brands are now exploring multi-functional tin formats with custom compartments, humidity control, and resealable child-resistant closures that elevate the user experience and align with emerging consumer preferences. Technological advancements such as smart packaging—including embedded QR codes, RFID chips, and NFC-enabled lids—open the door to interactive product tracking, supply chain traceability, and immersive storytelling via mobile applications. These features not only build trust and transparency but also differentiate products in a saturated market. Tin packaging also lends itself well to limited-edition runs and collectible designs, which foster consumer loyalty and drive repeat sales. Moreover, the industry’s growing emphasis on circular economy principles provides a platform for tin manufacturers to partner with retailers and dispensaries in take-back and recycling initiatives. By closing the material loop, brands can reduce environmental impact and reinforce their sustainability credentials.

Additionally, new printing and forming technologies, including digital and additive manufacturing, are lowering production costs and minimum order volumes, allowing small and boutique cannabis companies to participate in the tin packaging space. As legal cannabis markets expand and packaging technologies evolve, companies that prioritize smart design, regulatory compliance, and environmental performance will be best positioned to capitalize on the growing demand for premium, functional, and sustainable tin packaging solutions.

Segmental Overview

By Container Type

Based on Container Type, North America Tin Cannabis Packaging Market is segmented into Squeeze & Turn, twist-lid sealed tins, multi-use stash tins, custom printed collectible tins.

Twist-lid sealed tins currently dominate the North American tin cannabis packaging market due to their strong balance between functionality, compliance, and consumer appeal. These containers are widely adopted for products such as edibles, pre-rolls, and infused mints because they provide a secure seal that helps preserve aroma, flavor, and potency while protecting against external contaminants like moisture or light. Their compatibility with child-resistant mechanisms, including certified twist-and-push closures, makes them suitable across multiple state-level cannabis packaging regulations. Moreover, twist-lid tins are easy to manufacture in scalable volumes, offer excellent surface area for branding, and are relatively cost-effective compared to highly customized tins. They offer a sleek, familiar format that combines convenience with safety, which resonates with both recreational and medicinal cannabis users. Their availability in standard sizes further simplifies logistics, driving high-volume adoption among dispensaries and producers alike.

Custom printed collectible tins are the fastest growing segment in the North American tin cannabis packaging market, driven by the premiumization trend and demand for brand differentiation. As the cannabis market matures, especially in regions with dense competition, brands are increasingly turning to custom tin packaging to elevate perceived product value and create a lasting impression. These tins are used for limited-edition releases, seasonal collections, and collaborations, helping brands stand out on dispensary shelves. Collectible tins also appeal to environmentally conscious consumers who appreciate reusable packaging and often repurpose these containers, enhancing brand visibility post-purchase. The combination of aesthetics, sustainability, and emotional engagement—especially among lifestyle-oriented and wellness-conscious users—makes custom printed tins a powerful tool for marketing and loyalty-building. Technological advances in digital printing and low-volume customization have further enabled smaller brands to enter this space, fueling rapid growth.

By Distribution Channel

Based on Distribution Channel, the North America Tin Cannabis Packaging Market is segmented into Cannabis dispensaries, online marketplaces, manufacturing OEM packaging options. Cannabis dispensaries are the dominant distribution channel for tin cannabis packaging in North America. This is primarily because dispensaries serve as the primary point-of-sale for both recreational and medicinal cannabis products, especially in highly regulated markets like the United States and Canada. These retail outlets are bound by strict compliance requirements for packaging, including child resistance, product labeling, tamper evidence, and shelf-stability—criteria that tin packaging readily fulfills. Dispensaries prefer tin containers for products such as pre-rolls, infused edibles, and concentrates because they help enhance product presentation while ensuring regulatory adherence. In-store purchasing behavior also influences packaging choices; consumers are more likely to be attracted to visually appealing, premium-feeling containers like tins when shopping in physical locations OEM tin packaging suppliers. Furthermore, dispensaries frequently partner with premium brands that use collectible or custom-printed tins to drive brand differentiation and consumer loyalty. As a result, dispensaries remain the largest demand driver for tin packaging.

Online marketplaces are the fastest growing distribution channel for tin cannabis packaging, spurred by expanding e-commerce legalization in cannabis and changing consumer shopping habits. The COVID-19 pandemic accelerated online ordering trends, and many jurisdictions have since relaxed rules to allow direct-to-consumer cannabis deliveries. This shift has opened new opportunities for e-commerce-ready packaging—where tins offer a robust, tamper-proof, and visually appealing solution that protects product quality during transit. Brands are also investing in personalized, branded tin containers to create a premium unboxing experience, which is especially important in the online space where physical shelf presence is absent. Additionally, online channels enable a broader reach beyond local dispensaries, giving niche and boutique brands using tin packaging greater market access. The convenience of at-home ordering combined with rising consumer expectations for quality packaging is making online marketplaces a rapidly expanding channel for tin-based cannabis packaging solutions.

By End-User

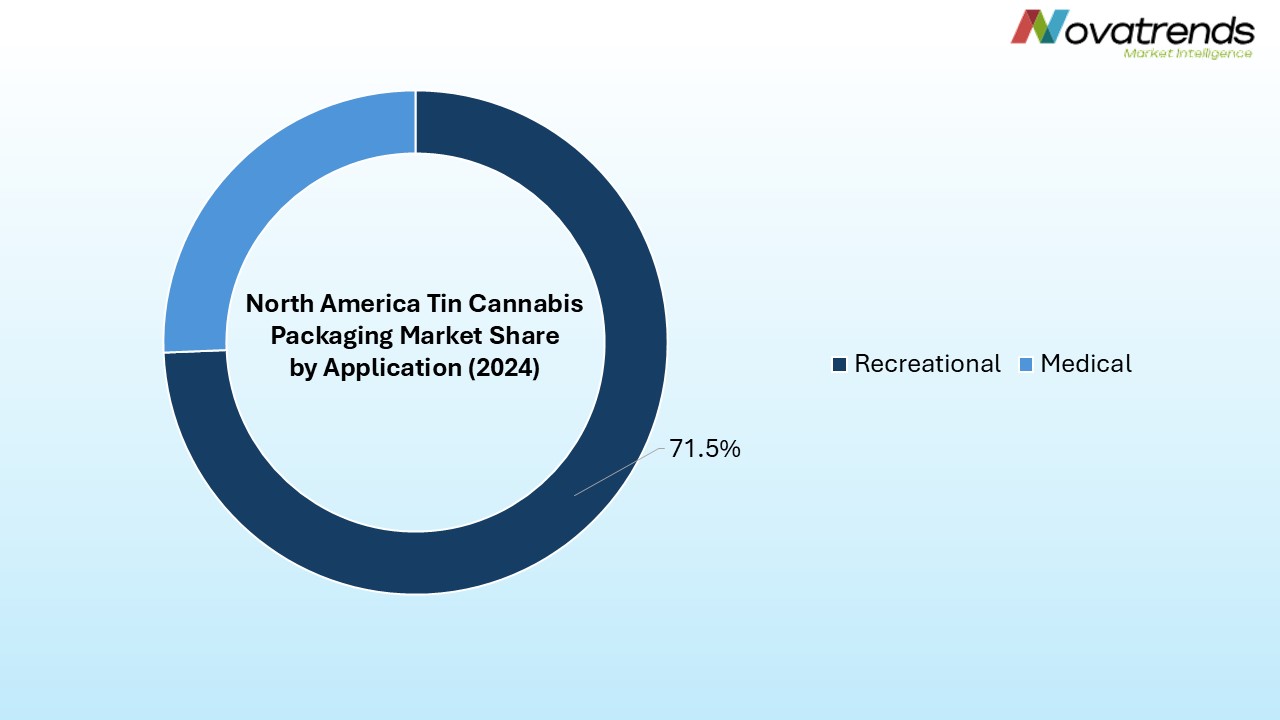

Based on End-User, the North America Tin Cannabis Packaging Market segmented into Recreational and Medical.

Recreational cannabis is the dominant end-user segment in the North America tin cannabis packaging market. This is largely due to the wider consumer base, broader product diversity, and more relaxed purchase volumes compared to the medical segment. In legalized states and Canada, the recreational market has experienced explosive growth, with a vast range of products—pre-rolls, edibles, concentrates, and vape cartridges—all requiring safe, attractive, and compliant packaging. Tin packaging is especially favored in this segment because of its premium look and feel, ability to support creative branding, and durability, which enhances the perceived value of lifestyle-oriented cannabis products. Since recreational consumers often base purchasing decisions on product appearance, convenience, and portability, tins offer a superior shelf presence compared to pouches or plastic containers. Additionally, the recreational space is highly competitive, pushing brands to differentiate through unique, custom-printed tin packaging that also meets regulatory standards such as child resistance and odor-proofing.

Medical cannabis is the fastest growing end-user segment for tin cannabis packaging in North America, driven by rising patient acceptance, expanding therapeutic applications, and increased regulatory standardization. As more healthcare providers and patients turn to cannabis for managing chronic pain, neurological disorders, and mental health conditions, the demand for consistent, safe, and hygienic packaging has grown. Tin packaging is gaining popularity in this segment due to its ability to preserve product integrity, prevent contamination, and support secure dosing through resealable, child-resistant designs. Moreover, the medical market places a premium cannabis packaging solutions on functionality and compliance, areas where tin packaging excels. Tins also offer better protection from light, air, and moisture compared to flexible packaging, which is critical for preserving the efficacy of medicinal cannabis over time. As governments expand medical programs and insurance frameworks begin to acknowledge cannabis-based therapies, the adoption of robust, pharmaceutical-grade packaging—like metal tins—is expected to accelerate rapidly in the coming years.

Country Overview

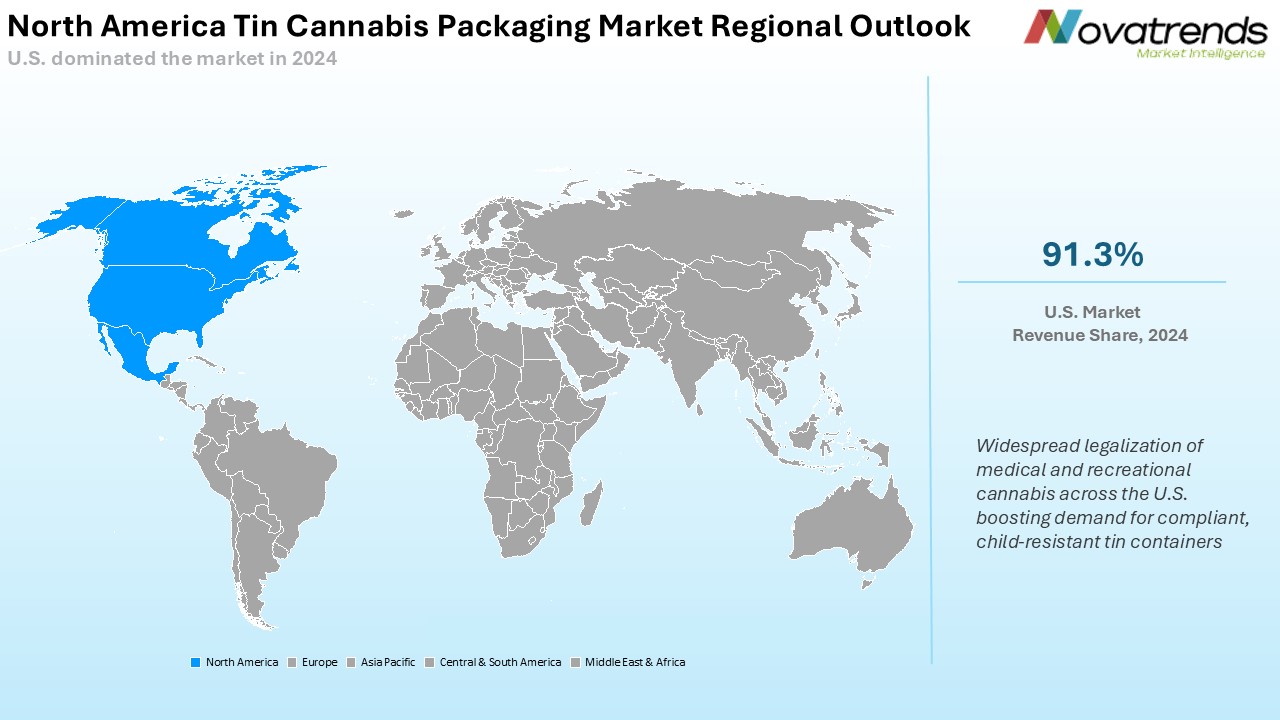

The United States dominates the North America tin cannabis packaging market, primarily due to its large and rapidly expanding cannabis industry. While cannabis remains federally illegal, more than half of the U.S. states have legalized it for medical and/or recreational use, creating a highly active and fragmented market. The scale and maturity of this industry generate significant demand for compliant, tamper-proof, and visually appealing packaging solutions—areas where tin packaging excels. U.S. cannabis brands are also at the forefront of packaging innovation, heavily investing in premiumization and branding to capture market share. Tins are widely adopted for their customizable surfaces, durability, and child-resistant features, especially in high-growth product categories like pre-rolls, edibles, and concentrates. The country's well-established dispensary networks, combined with e-commerce delivery options in several states, further fuel the demand for high-quality tins that protect and market the product simultaneously. U.S. regulatory frameworks also mandate strict packaging compliance, making tins a favorable choice among manufacturers and retailers.

The Canadian cannabis packaging market is experiencing steady growth, driven by expanding demand for both recreational and medical cannabis products. Rigid packaging formats such as tins, bottles, and jars continue to dominate due to their durability, regulatory compliance, and suitability for child-resistant and tamper-evident designs mandated under Canada's Cannabis Act. However, there is a growing shift toward flexible packaging options as brands seek cost-efficiency and improved shelf appeal. The market is also witnessing increased adoption of sustainable and eco-friendly materials in response to consumer preferences and environmental policies. Innovation in packaging is further accelerated by the rising popularity of pre-rolls, edibles, and infused products, necessitating specialized, compliant formats. Overall, the Canadian cannabis packaging market is poised for consistent double-digit growth through the latter half of the decade, shaped by evolving regulations, sustainability trends, and product diversification.

Mexico is the fastest growing country in the North America tin cannabis packaging market, largely due to its ongoing regulatory transformation. The country is in the process of legalizing cannabis for adult use following the Supreme Court’s mandate to decriminalize it, which has opened the door for formal legislation and market development. While the market is still in early stages compared to the U.S. and Canada, the potential for rapid growth is high as businesses prepare for legal commercial operations. As the regulatory framework matures, demand for compliant and secure packaging—especially metal tins for branding, preservation, and safety—will increase sharply. Additionally, cannabis tin packaging manufacturers looking to expand into emerging Latin American markets view Mexico as a strategic entry point. Local and international brands are already exploring packaging partnerships and import routes to position themselves early in the market. This evolving legal landscape, combined with a growing consumer base and regulatory alignment, positions Mexico as the fastest growing segment in the regional tin packaging market.

Competitive Landscape

The North American tin cannabis packaging market is highly fragmented, characterized by a mix of specialty cannabis-focused suppliers and larger metal-container conglomerates competing on customization, compliance, and sustainability. Established names such as PakFactory, Marijuana Packaging, Compliant Packaging, Tin King USA, and Berlin Packaging dominate high-volume orders with child-resistant, tamper-evident tins that meet strict state and provincial rules, while traditional metal giants like Crown Holdings supply industrial-scale tinplate and leverage deep manufacturing expertise.

Mid-sized innovators—including Treeform, GPA Global, Dymapak, and Ztoda—differentiate through eco-friendly alloys, zero-solvent inks, and rapid digital printing that enable limited runs for craft brands. Niche players such as Cannaline, Green Rush Packaging, KacePack, CRATIV Packaging, and RXDco emphasize speed-to-market programs and collectible tins that align with premiumization trends. Competitive pressure centers on offering turnkey, fully certified packaging that balances upscale branding with cost control, especially as tariffs on imported metal raise raw-material prices. Mergers, acquisitions, and strategic partnerships are intensifying—exemplified by Berlin Packaging’s cannabis-specific expansions—as companies seek scale, regional compliance expertise, and sustainable cannabis tin containers innovation to secure long-term contracts in a market driven by consumer preference for recyclable, visually striking, and regulatory-ready tin solutions.

Key Market Players

- PakFactory

- Marijuana Packaging

- Smoke Cones

- SKS Bottle & Packaging, Inc.

- Compliant Packaging, LLC

- Tin King USA

- Tin Canna

- Ztoda Packaging

- Treeform Packaging Solutions

- Tinwonder

- DC Packaging

- Marijuana Packaging Solution (distinct from Marijuana Packaging)

- Berk

- Berlin Packaging

- The Bureau

Major Industry Updates

The North American tin cannabis packaging market has seen several notable developments shaping its growth trajectory. A major trend is the increasing demand for high-capacity tin formats, such as multi-pack pre-roll tins, which cater to large-scale operators seeking efficiency, compliance, and enhanced shelf presence. These designs are being adopted widely across dispensaries and wholesale cannabis packaging channels due to their durability, child-resistant features, and ability to carry detailed regulatory labeling. Additionally, the market is experiencing significant growth fueled by the broader legalization of cannabis across U.S. states and the expansion of product lines within recreational and medical use categories.

- In June 2025, The Packaging Company launched a new 28‑pack pre‑roll tin for high‑volume cannabis operations. This durable, rigid metal tin accommodates up to 28 standard 109 mm pre-rolls and meets child‑resistant, tamper‑evident, odor- and moisture-control standards. It provides ample label space, recyclable materials, and streamlined logistics compliance.

- In March 2025, Sana Packaging has reduced prices on its core Made‑in‑the‑USA cannabis packaging by up to 15%, effective immediately. This strategic move aims to support customers amid unpredictable tariffs and supply‑chain disruptions. By offering affordable, sustainable packaging domestically, Sana reinforces its commitment to eco‑friendly solutions without compromising quality.

- In June 2024, Contempo Specialty Packaging has launched a sustainable, compostable flower-pod system for cannabis. The system includes a reusable, child-resistant metal tin and a single-use, home‑ and industrial‑compostable pod made from certified biobased resin. Initial purchases include both components; future refills consist only of the pod—reducing waste and sterilization impacts.

- In June 2024, Grove Bags has launched ExIce, the first fully water‑soluble, eco‑friendly storage solution for fresh‑frozen cannabis. Designed to prevent freezer burn and UV damage, it dissolves completely without microplastics, offering antimicrobial, anti‑static protection in sub‑zero environments—preserving terpene integrity while ensuring marine-safe biodegradability.

- In December 2022, Hoffmann Neopac has introduced a fully metal, child-resistant tin designed for dry and semi-dry cannabis products, including edibles and oils. Made entirely from recyclable metal, it offers high barrier protection, tamper-evidence, and safety compliance, combining sustainability with regulatory-ready design.

North America Tin Cannabis Packaging Market Report- Scope (Customizable)

Scope |

Description |

|

Historic Period |

2018-2023 |

|

Base Year (Esti.) |

2024 |

|

Forecast Period (F) |

2025-2035 |

|

Market Revenue |

USD Million |

|

Market by Container Type |

Squeeze & Turn, twist-lid sealed tins, multi-use stash tins, custom printed collectible tins |

|

Market by Distribution Channel |

Cannabis dispensaries, online marketplaces, manufacturing OEM packaging options |

|

Market by End-user |

Recreational and Medical |

|

Countries Covered |

U.S., Canada, Mexico |

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?