Market Overview

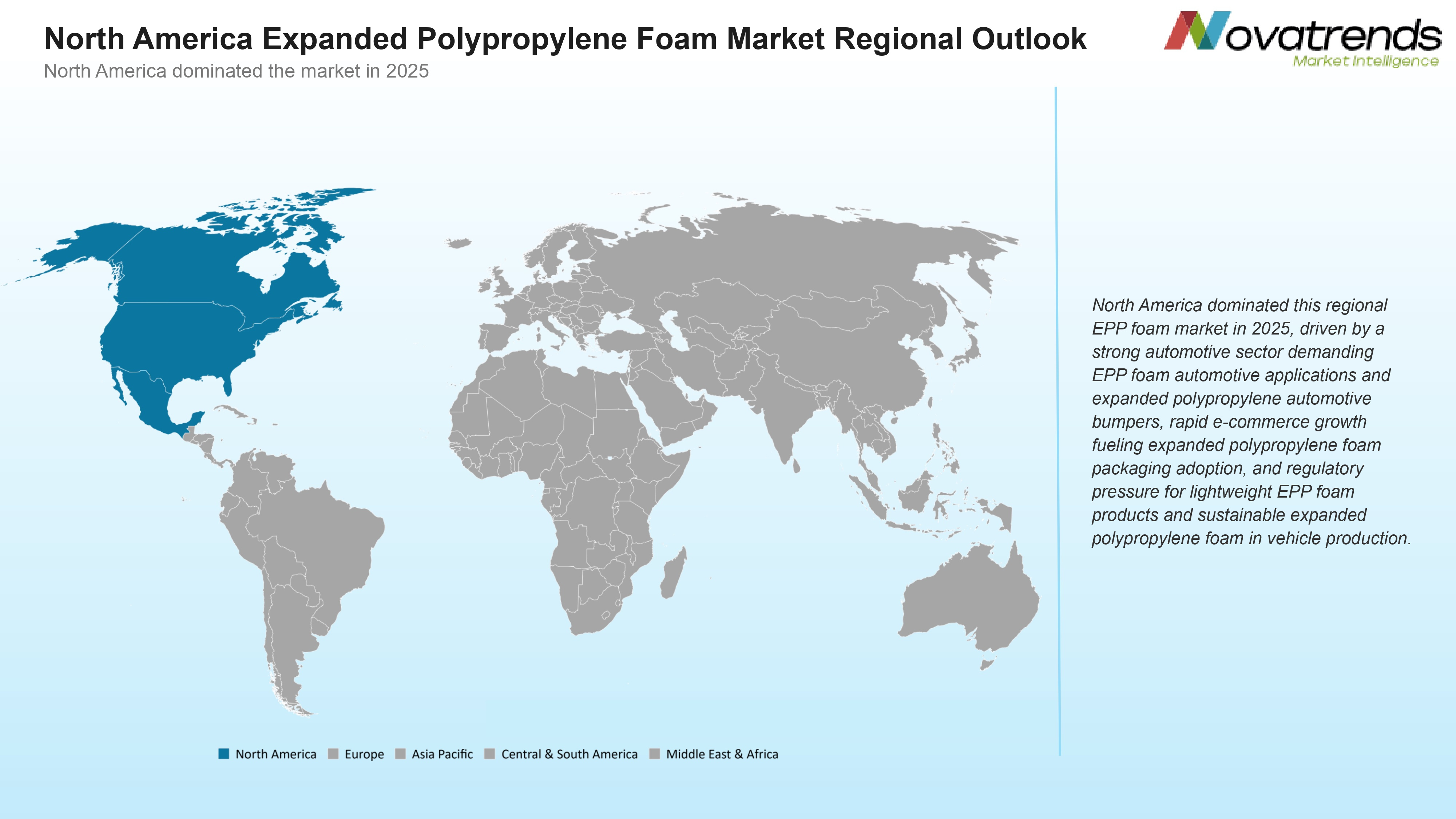

According to Novatrends Market Intelligence, the North America Expanded Polypropylene Foam Market was valued at USD 1.8 billion in 2025 and is anticipated to propel at a growth rate of 6.1% from 2026-2036.

Expanded polypropylene (EPP) foam is a high-performance closed-cell foam material valued for its lightweight EPP foam products characteristics, EPP foam impact absorption performance, and EPP foam thermal insulation properties. Expanded polypropylene foam packaging is widely used for EPP foam for electronics packaging and EPP foam medical device packaging, providing superior protection-to-weight ratios. EPP foam automotive applications are the largest end-use segment, encompassing expanded polypropylene automotive bumpers, EPP foam child safety seats, and door panel energy absorbers driving adoption from OEMs pursuing vehicle lightweighting. Custom molded EPP foam products serve niche applications from EPP foam for sports equipment to EPP foam buoyancy applications in marine products, while EPP foam reusable packaging is growing with sustainability-driven supply chain redesigns. Sustainable expanded polypropylene foam and expanded polypropylene foam recycling capabilities further reinforce the material's circular economy credentials.

Market Dynamics

The market is driven by automotive lightweighting requirements accelerating EPP foam automotive applications, growing e-commerce driving expanded polypropylene foam packaging demand, and rising EPP foam for consumer electronics in device protection. EPP foam construction applications in impact-resistant insulation panels are emerging alongside EPP foam for sports equipment in helmets, knee pads, and water floatation devices. Expanded polypropylene foam density engineering enables application-specific performance optimization, while molded EPP foam components allow complex geometries for automotive interiors. In March 2024, JSP International expanded custom molded EPP foam products capacity in North America targeting EPP foam automotive applications and EPP foam child safety seats for U.S. OEMs. Sustainable expanded polypropylene foam and expanded polypropylene foam recycling programs are growing as brands pursue circular packaging commitments for EPP foam reusable packaging systems across North American supply chains.

Segment Analysis

By Density: Below 30 g/L holds the largest share of the North America Expanded Polypropylene Foam market, supported by strong adoption and well-established supply chains across key end-use industries. 30–60 g/L is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Application: Automotive holds the largest share of the North America Expanded Polypropylene Foam market, supported by strong adoption and well-established supply chains across key end-use industries. Packaging is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By End-Use Industry: Automotive holds the largest share of the North America Expanded Polypropylene Foam market, supported by strong adoption and well-established supply chains across key end-use industries. Electronics is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

Recent Developments in North America EPP Foam Market

- In February 2024, JSP International expanded North American custom molded EPP foam products capacity at its Michigan facility, targeting EPP foam automotive applications including expanded polypropylene automotive bumpers and EPP foam child safety seats for major U.S. and Canadian OEMs.

- In May 2024, Kaneka Corporation introduced new sustainable expanded polypropylene foam grades for EPP foam reusable packaging, featuring expanded polypropylene foam recycling compatibility and EPP foam for electronics packaging applications with enhanced EPP foam impact absorption for e-commerce logistics.

- In August 2024, Woodbridge Group launched EPP foam construction applications panels for wall insulation and roof decking, featuring expanded polypropylene foam insulation performance and lightweight EPP foam products for commercial building construction in North America.

- In October 2024, Foam Fabricators Inc. expanded EPP foam medical device packaging and EPP foam for consumer electronics product lines, focusing on custom molded EPP foam products with expanded polypropylene foam density optimization for sensitive device protection.

- In January 2025, Pregis Corporation launched EPP foam for sports equipment and EPP foam buoyancy applications product lines, targeting North American sporting goods OEMs and marine safety equipment manufacturers requiring lightweight EPP foam products with superior performance.

- In March 2025, Sonoco Products introduced EPP foam reusable packaging systems for automotive parts and expanded polypropylene foam packaging for pharmaceutical cold chain logistics, featuring sustainable expanded polypropylene foam and expanded polypropylene foam recycling take-back programs.

Top North America Expanded Polypropylene Foam Market - Key Market Players

- JSP International

- Kaneka Corporation

- Woodbridge Group

- Foam Fabricators Inc.

- Pregis Corporation

- Sonoco Products

- NCI Information Systems

- Zotefoams plc

- Sealed Air Corporation

- Coda Plastics Ltd.

- Universal Forest Products

- ACH Foam Technologies

- Leggett & Platt

- UFP Technologies

- Premier Industries

Global North America Expanded Polypropylene Foam Market Report- Scope (Customizable)

Scope | Description |

Historic Period | 2021-2024 |

Base Year (Esti.) | 2025 |

Forecast Period (F) | 2026-2036 |

Market Values | USD Billion |

By Density | Below 30 g/L, 30–60 g/L, Above 60 g/L |

By Application | Automotive, Packaging, Consumer Electronics, Construction |

By End-Use Industry | Automotive, Electronics, Packaging, Sports & Recreation |

Market by Region | North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

Countries Covered | U.S., Canada, and Mexico; Germany, France, UK, Russia, Italy, Spain, and Netherlands; China, India, Japan, South Korea, and Australia; Brazil, Argentina; Saudi Arabia, UAE, Turkey, Egypt, and South Africa |

Detailed Market Segmentation

- By Density (Revenue in USD Million)

- Below 30 g/L

- 30–60 g/L

- Above 60 g/L

- By Application (Revenue in USD Million)

- Automotive

- Packaging

- Consumer Electronics

- Construction

- By End-Use Industry (Revenue in USD Million)

- Automotive

- Electronics

- Packaging

- Sports & Recreation

- By Region (Revenue in USD Million)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Russia

- Italy

- Spain

- Netherlands

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Central & South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Egypt

- South Africa

- North America

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?