Market Overview

According to Novatrends Market Intelligence, the Global Non-Volatile Memory Market was valued at USD 98.4 billion in 2025 and is anticipated to propel at a growth rate of 9.1% from 2026-2036.

The global non-volatile memory market is a foundational segment of the semiconductor industry, retaining data without power across consumer electronics, enterprise storage, automotive electronics, and industrial IoT applications. NAND Flash — particularly 3D NAND — dominates non volatile memory market revenue, enabling SSDs and embedded storage at continuously declining cost per bit. NOR Flash serves code storage in microcontrollers and automotive electronics, while EEPROM remains standard for small-footprint data retention. Next generation non volatile memory technologies including MRAM (Magnetoresistive RAM), PCM (Phase Change Memory), ReRAM (Resistive RAM), and FeRAM (Ferroelectric RAM) are emerging non volatile memory technologies addressing the performance, endurance, and power limitations of conventional NAND. Advanced memory technologies are being driven by AI accelerator requirements for fast, dense, energy-efficient non volatile memory market solutions. The global non volatile memory market is characterized by high capital intensity, cyclical pricing, and concentrated production among Samsung, SK Hynix, Micron, and Kioxia/Western Digital. Non volatile memory market demand from cloud hyperscalers, edge computing, and automotive AI is sustaining long-term growth across all non volatile memory market segmentation categories.

Market Dynamics

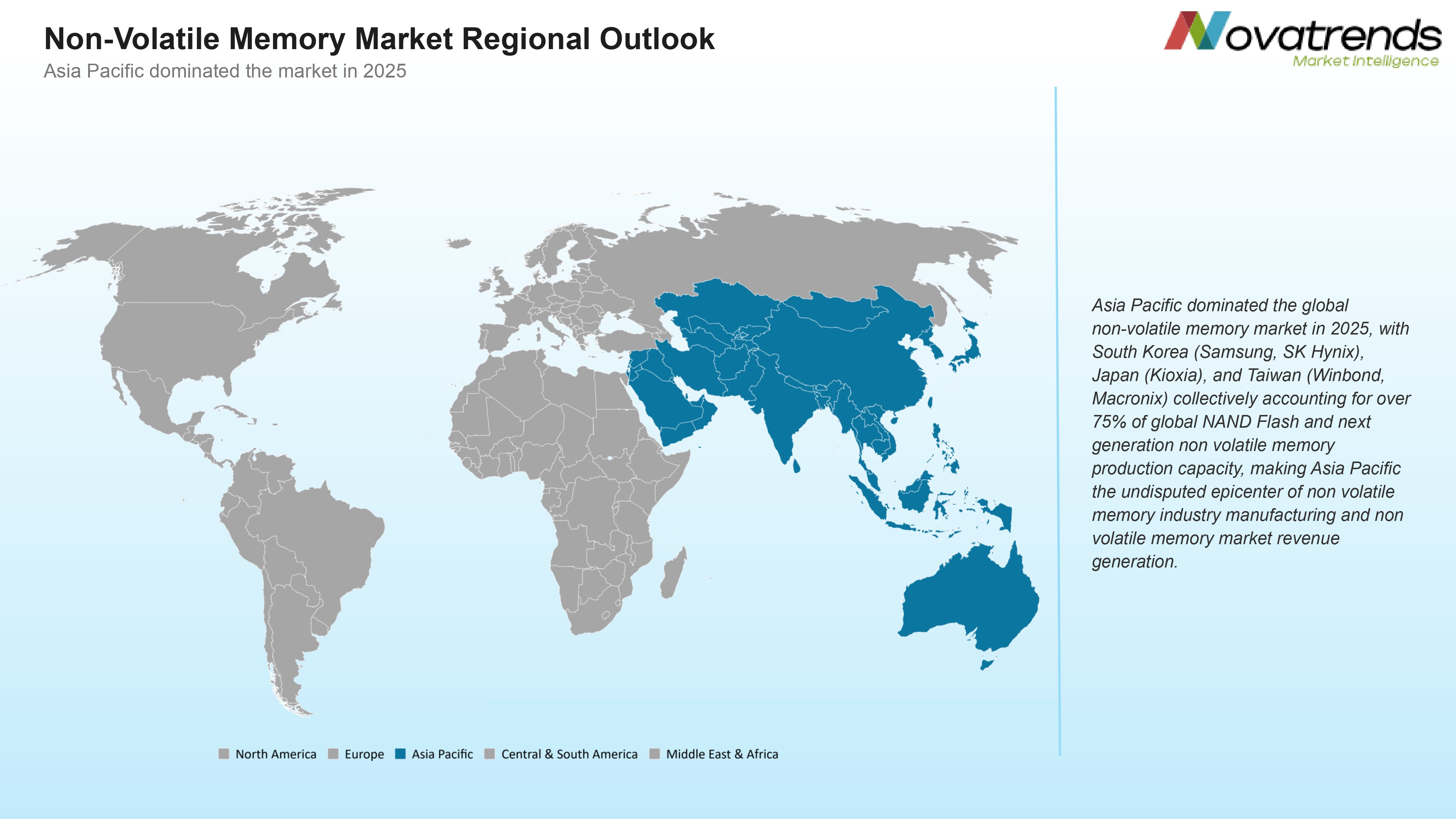

Non volatile memory market drivers include AI model training and inference expanding enterprise SSD demand, automotive ADAS and connected vehicle platforms requiring high-reliability non volatile memory industry solutions, and IoT device proliferation creating billions of new embedded non volatile memory demand points. Non volatile memory market challenges include supply-demand cycle volatility, high capital investment requirements for leading-edge 3D NAND fab capacity, and the technical complexity of transitioning from planar to next generation non volatile memory 3D architectures. Non volatile memory market opportunities are significant in AI edge inference hardware, autonomous vehicle systems, and industrial automation requiring emerging non volatile memory technologies with superior endurance. Non volatile memory market regional analysis shows Asia Pacific leading production while North America leads advanced memory technologies design. In January 2024, Samsung Electronics expanded 3D NAND and next generation non volatile memory capacity targeting AI server SSD demand, while Micron Technology announced next generation non volatile memory NAND for data center applications. Non volatile memory market competitive landscape consolidation, non volatile memory market size expansion driven by AI server and edge computing demand, and non volatile memory market trends toward chiplet integration and near-memory computing are shaping global non volatile memory market forecast through 2036.

Segment Analysis

By Technology: NAND Flash (3D NAND) holds the largest share of the Non-Volatile Memory market, supported by strong adoption and well-established supply chains across key end-use industries. NOR Flash is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Application: Consumer Electronics holds the largest share of the Non-Volatile Memory market, supported by strong adoption and well-established supply chains across key end-use industries. Enterprise Storage is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Form Factor: SSD holds the largest share of the Non-Volatile Memory market, supported by strong adoption and well-established supply chains across key end-use industries. Embedded is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

Recent Developments in Non-Volatile Memory Market

- In January 2024, Samsung Electronics expanded 3D NAND production targeting advanced memory technologies for AI server SSD non volatile memory market demand, advancing next generation non volatile memory with 9th generation V-NAND featuring 290+ layer stacking and improved non volatile memory market CAGR for enterprise applications.

- In April 2024, Micron Technology launched 232-layer NAND Flash advanced memory technologies and next generation non volatile memory solutions for data center SSDs, driving non volatile memory market growth with best-in-class storage density and non volatile memory market revenue improvement for hyperscaler customers.

- In July 2024, Everspin Technologies expanded emerging non volatile memory technologies MRAM production, delivering next generation non volatile memory solutions for industrial IoT, automotive, and enterprise applications requiring ultra-high endurance advanced memory technologies beyond NAND capabilities.

- In September 2024, SK Hynix advanced non volatile memory industry trends with 238-layer NAND and HBM3E DRAM, positioning for non volatile memory market opportunities in AI accelerator memory stacks and announcing next generation non volatile memory investment for non volatile memory market growth in Korean and North American fab expansion.

- In December 2024, Kioxia (Toshiba Memory) launched new 3D NAND and emerging non volatile memory technologies platforms for global non volatile memory market competitive landscape positioning, targeting non volatile memory market demand from enterprise, automotive, and consumer electronics non volatile memory market segmentation categories.

- In March 2025, Intel Corporation advanced non volatile memory market outlook with Optane-successor emerging non volatile memory technologies and NAND technology licensing, addressing non volatile memory market challenges in the data center storage tier with advanced memory technologies enabling tiered memory architectures for AI workloads.

Top Non-Volatile Memory Market - Key Market Players

- Samsung Electronics

- Micron Technology

- SK Hynix

- Kioxia Corporation

- Western Digital Corporation

- Intel Corporation

- Everspin Technologies

- Winbond Electronics

- Macronix International

- ISSI (Integrated Silicon Solution)

- Microchip Technology

- Infineon Technologies

- Renesas Electronics

- STMicroelectronics

- Onsemi

Global Non-Volatile Memory Market Report- Scope (Customizable)

Scope | Description |

Historic Period | 2021-2024 |

Base Year (Esti.) | 2025 |

Forecast Period (F) | 2026-2036 |

Market Values | USD Billion |

By Technology | NAND Flash (3D NAND), NOR Flash, EEPROM, MRAM, PCM, ReRAM |

By Application | Consumer Electronics, Enterprise Storage, Automotive, Industrial, IoT |

By Form Factor | SSD, Embedded, Removable |

Market by Region | North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

Countries Covered | U.S., Canada, and Mexico; Germany, France, UK, Russia, Italy, Spain, and Netherlands; China, India, Japan, South Korea, and Australia; Brazil, Argentina; Saudi Arabia, UAE, Turkey, Egypt, and South Africa |

Detailed Market Segmentation

- By Technology (Revenue in USD Million)

- NAND Flash (3D NAND)

- NOR Flash

- EEPROM

- MRAM

- PCM

- ReRAM

- By Application (Revenue in USD Million)

- Consumer Electronics

- Enterprise Storage

- Automotive

- Industrial

- IoT

- By Form Factor (Revenue in USD Million)

- SSD

- Embedded

- Removable

- By Region (Revenue in USD Million)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Russia

- Italy

- Spain

- Netherlands

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Central & South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Egypt

- South Africa

- North America

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?