Marine Lubricants Market Report Overview

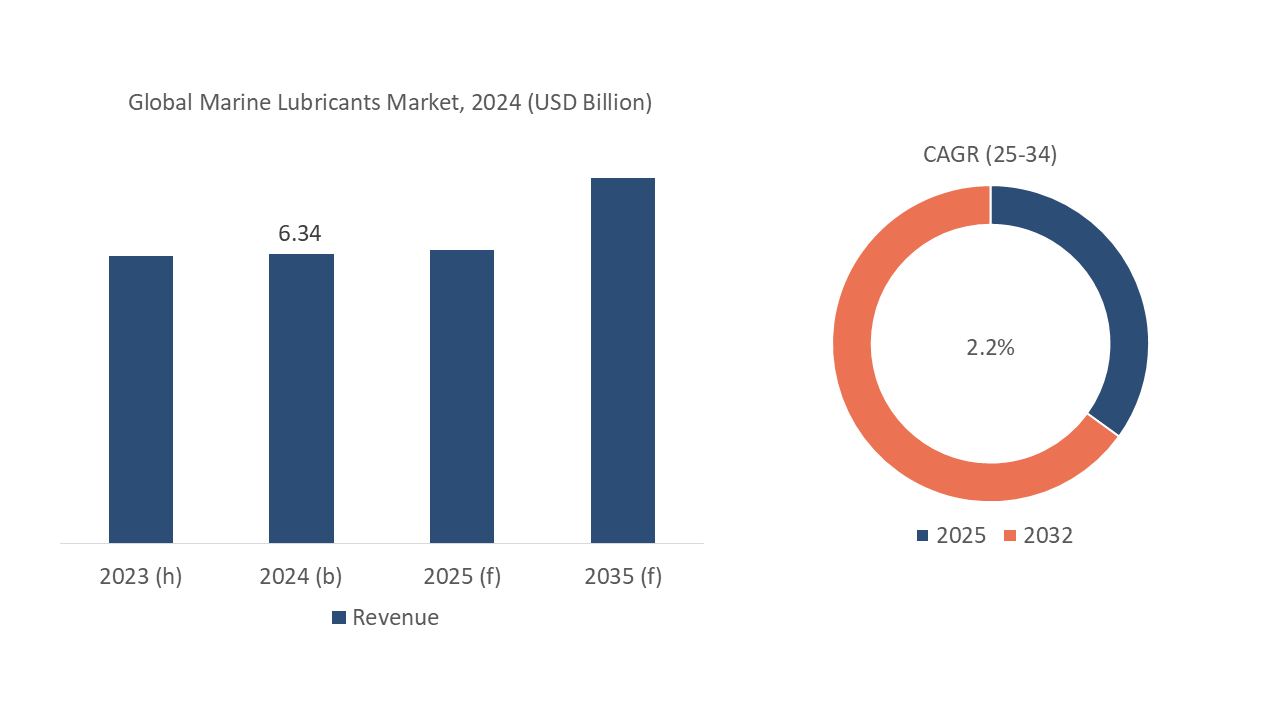

According to Novatrends Market Intelligence, the global marine lubricants Market was valued at USD 6.34 billion in 2024 and is anticipated to propel at a growth rate of 2.20% from 2025-2032. The marine lubricants market is primarily driven by the global expansion of the shipping industry, which has experienced significant growth due to rising international trade and demand for raw materials and goods. As shipping volumes increase, so does the need for efficient vessel maintenance, where marine lubricants play a crucial role in ensuring engine reliability and reducing friction and wear. Additionally, stringent environmental regulations imposed by bodies such as the International Maritime Organization (IMO) have encouraged the development of eco-friendly, biodegradable lubricants that help reduce harmful emissions and meet compliance standards.

Innovations in lubricant formulations, aimed at improving fuel efficiency and extending the operational life of marine engines, are further supporting market growth. The ongoing shift towards cleaner fuels, such as LNG and low-sulfur fuels, requires specialized lubricants, creating new market opportunities. Moreover, the rising demand for leisure and commercial vessels, coupled with increasing awareness of preventive maintenance, contributes to the expanding consumption of marine lubricants. However, fluctuations in crude oil prices, which influence the cost of raw materials for lubricant production, pose a potential challenge to the market. In addition, the push for more sustainable practices and the adoption of alternative propulsion technologies, such as electric and hybrid systems, may reshape demand patterns in the long term.

Marine Lubricants Market Recent Developments

Marine lubricants market is anticipated to propel at a compounded annual growth rate (CAGR) of 2.20% from 2025-2032. Recent developments in the marine lubricants market have been largely shaped by increasing environmental regulations and technological advancements.

Companies such as Shell, ExxonMobil, and Chevron have introduced new product lines with improved formulations that enhance fuel efficiency and reduce engine wear. There’s been a focus on the development of synthetic lubricants, which offer better performance in extreme conditions and longer oil life, contributing to cost savings for operators. These trends underscore the industry's focus on sustainability, efficiency, and compliance with evolving regulatory standards. For instance,

- In September 2024, Maxol Lubricants unveiled a new product line of greases specifically developed to cater to the changing requirements of various sectors, such as agriculture, farming, marine, and forestry. This range is especially formulated for the lubrication of plain bearings, wire ropes, chains, rails, and gear systems across a wide variety of equipment.

- In April 2024, Castrol, a prominent global lubricant brand, introduced its updated Castrol TLX product range, now tailored for medium-speed four-stroke engines. This newly reformulated range will replace the previous Castrol TLX Xtra and TLX Plus fluids, offering enhanced versatility to accommodate a wider array of engine types and applications, all while maintaining superior engine protection, reliability, and performance.

- In October 2023, Gulf Oil Middle East unveiled a new product line which includes Gulf Super Fleet Professional, Gulf Super Fleet Supreme, and Gulf Super Fleet Duty, all designed to enhance fuel efficiency, extend drain intervals, reduce vehicle downtime, and lower maintenance costs.

Regional Overview

Asia Pacific dominated the global marine lubricants market in 2024 with a market revenue share of 27.76%. Recent developments in the Asia Pacific marine lubricants market have been driven by the region’s booming maritime trade and the growing influence of environmental regulations. As major ports in countries like China, Japan, South Korea, and Singapore handle increasing cargo volumes, the demand for high-performance marine lubricants has surged.

The implementation of the IMO 2020 sulfur cap has prompted ship operators in the region to adopt low-sulfur fuels, driving demand for compatible lubricants. Additionally, key players in the Asia Pacific market, including companies like TotalEnergies, BP, and Sinopec, are focusing on expanding their portfolios of environmentally acceptable lubricants (EALs) and bio-based solutions to cater to the growing demand for sustainable products.

Digital solutions for real-time lubricant monitoring and predictive maintenance are also gaining traction among regional fleet operators, aimed at reducing downtime and optimizing performance. Furthermore, the region is witnessing increased investment in research and development to formulate advanced synthetic lubricants that offer enhanced protection for marine engines, even in harsh operating conditions common in Asia’s busy shipping routes.

U.S. Marine Lubricants Market Overview

The U.S. marine lubricants market is characterized by steady growth, driven by the country's extensive maritime trade activities, robust naval operations, and the presence of large commercial shipping fleets along key ports. As one of the world’s largest importers and exporters, the U.S. relies heavily on marine transport, fueling demand for high-performance lubricants that ensure engine reliability and efficiency. The market is also influenced by stringent environmental regulations from agencies like the Environmental Protection Agency (EPA) and adherence to International Maritime Organization (IMO) standards, pushing for the adoption of low-sulfur fuels and eco-friendly lubricants.

Major players in the U.S., such as Chevron, ExxonMobil, and Shell, are continuously developing advanced formulations, including synthetic and biodegradable lubricants, to meet evolving operational and environmental requirements. Moreover, the growing emphasis on reducing greenhouse gas emissions and improving fuel efficiency has spurred innovations in lubricant technology. While the market is mature, challenges like fluctuating crude oil prices and increased adoption of alternative propulsion technologies (electric and hybrid systems) may impact future demand for traditional marine lubricants.

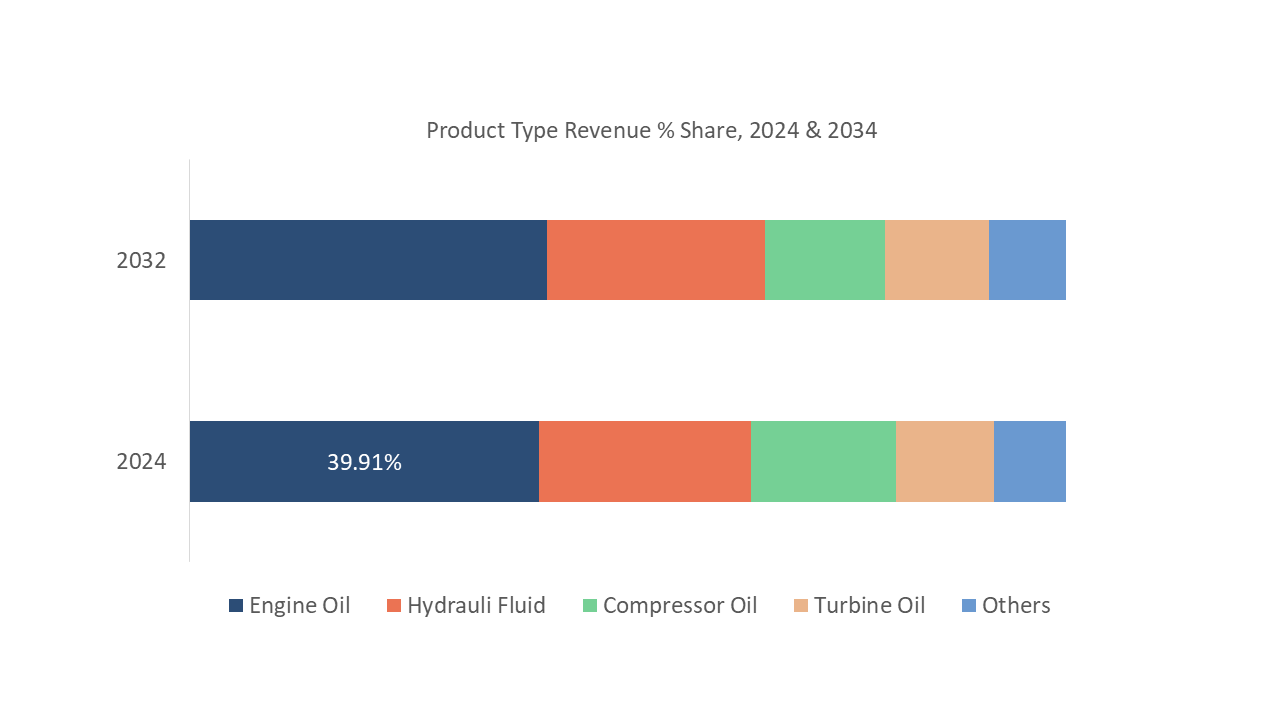

Product Type Overview

Engine Oil dominated the product type segmentation across the global marine lubricants market in 2024 with a market revenue share of 39.91%. The engine oil marine lubricants market is experiencing steady growth, driven by the expansion of global maritime trade and increasing demand for high-performance lubricants to maintain vessel efficiency.

Advancements in synthetic engine oils, which offer superior thermal stability, longer service intervals, and better protection in extreme conditions, are further fueling market growth. The rising focus on sustainability has also boosted the development and adoption of environmentally friendly and biodegradable lubricants. As maritime fleets grow and modernize, particularly in regions like Asia Pacific, North America, and Europe, the engine oil segment of marine lubricants is expected to see continued expansion.

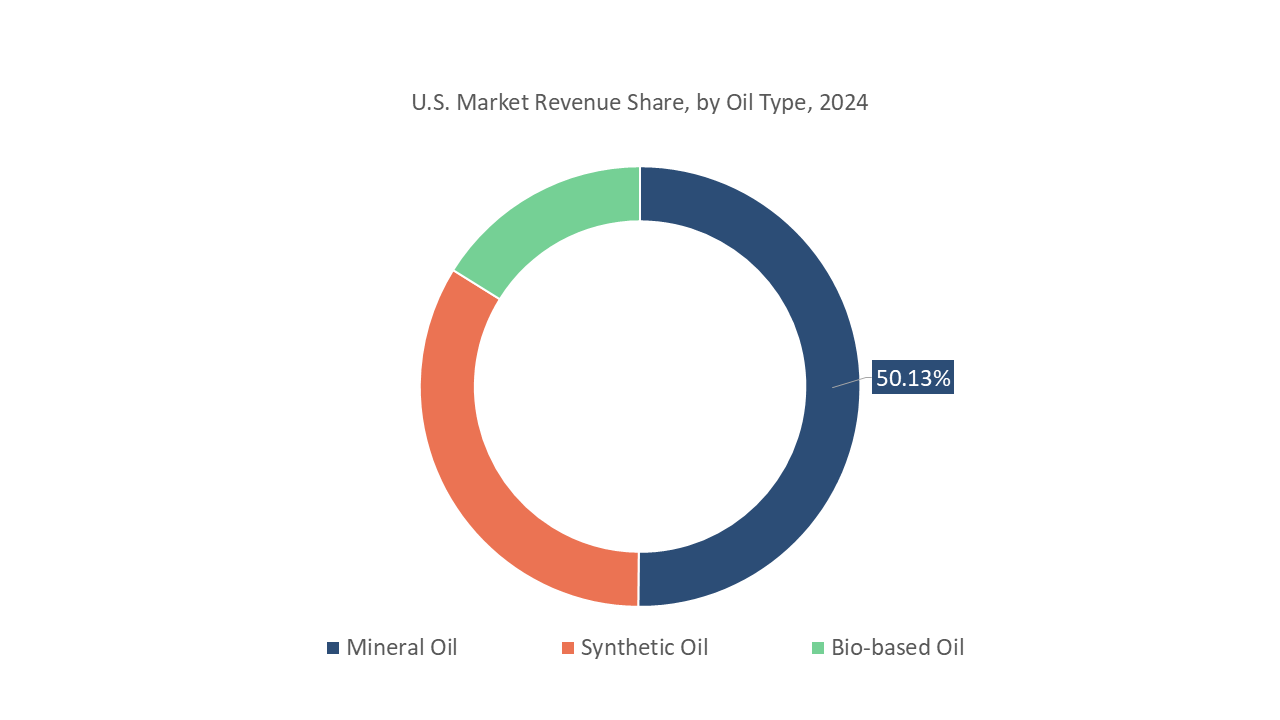

Oil Type Overview

Mineral Oil dominated the oil type segmentation across the global marine lubricants market in 2024 with a market revenue share of 48.56%. The mineral oil marine lubricants market is witnessing moderate growth, largely driven by the continued use of traditional vessels and engines that rely on cost-effective lubricants. While the market faces competition from synthetic and biodegradable alternatives, mineral oil-based lubricants remain widely used due to their affordability and availability, particularly in older ships and less regulated regions.

The increasing global shipping activity, especially in emerging markets, is supporting demand for these lubricants. However, the market is being shaped by environmental regulations such as the International Maritime Organization’s (IMO) sulfur cap, which is pushing operators to adopt cleaner fuel types and lubricants with lower environmental impacts.

As a result, the development of low-sulfur-compatible mineral oil lubricants has become a focal point for manufacturers. Growth in this market is expected to be stable but may slow down in the future as the industry shifts towards more eco-friendly and advanced synthetic lubricants, driven by the demand for higher performance and environmental compliance.

Vessel Type Overview

Bulk Carriers dominated the Vessel Type segmentation across the global Marine Lubricants Market in 2023 with a market revenue share of 48.52%. The marine lubricants market in the bulk carrier segment is experiencing growth due to the increasing global demand for raw materials like coal, iron ore, and grain, which are primarily transported by these vessels. As the bulk carrier fleet expands to meet rising global trade, the need for high-performance lubricants to maintain engine efficiency, reduce wear, and ensure smooth operation has surged.

Additionally, regulatory changes such as the International Maritime Organization’s (IMO) 2020 sulfur cap have spurred demand for lubricants compatible with low-sulfur and alternative fuels. Innovations in lubricant technology, such as the development of synthetic and biodegradable marine lubricants, are becoming more prominent as ship operators seek to comply with environmental regulations while optimizing vessel performance.

Moreover, the focus on fuel efficiency and reducing operating costs is encouraging the use of advanced lubricants that extend maintenance intervals and improve engine life. The Asia Pacific region, home to some of the world’s largest bulk carriers and trade routes, is a key driver of this market's growth.

Market Characteristics

The marine lubricants market is characterized by a diverse product range tailored to meet the specific demands of various vessel types, including engine oils, hydraulic fluids, gear oils, and greases. It operates in a highly regulated environment, with stringent global standards, such as the International Maritime Organization’s (IMO) sulfur cap, pushing for environmentally compliant and low-sulfur-compatible lubricants. The market is heavily influenced by the shipping industry’s need for high-performance, durable lubricants that optimize engine efficiency, reduce wear, and extend maintenance intervals, especially in harsh marine conditions.

It is also shaped by technological advancements, including synthetic and biodegradable lubricants, which offer superior protection, longer oil life, and lower environmental impact compared to traditional mineral-based products. Additionally, regional dynamics play a significant role, with major growth seen in Asia Pacific due to its dominance in global maritime trade. The market is highly competitive, with major players like Shell, ExxonMobil, and Chevron continually innovating to meet evolving environmental regulations and performance needs. The increasing adoption of digital monitoring systems for real-time lubricant performance tracking is also a growing trend within the market.

Global Marine Lubricants Market Report- Scope (Customizable)

| Scope | Description |

| Historic Period | 2018-2023 |

| Base Year (Esti.) | 2024 |

| Forecast Period (F) | 2025-2032 |

| Market Revenue | USD Million |

| Market by Product Type | Engine Oil, Hydraulic Fluid, Compressor Oil |

| Market by Oil Type | Mineral Oil, Synthetic Oil, Bio-based Oil |

| Market by Vessel Type | Bulk Carriers, Tankers, Container Ships and Others |

| Market by Region | North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

| Countries Covered | U.S., Canada, Mexico; Germany, UK, Italy, France, Spain; China, India, Japan, South Korea, Malaysia, Singapore, Thailand, Vietnam, Australia & New Zealand; Brazil, Argentina; Saudi Arabia, United Arab Emirates (UAE), South Africa |

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?