Iron Casting Market Overview

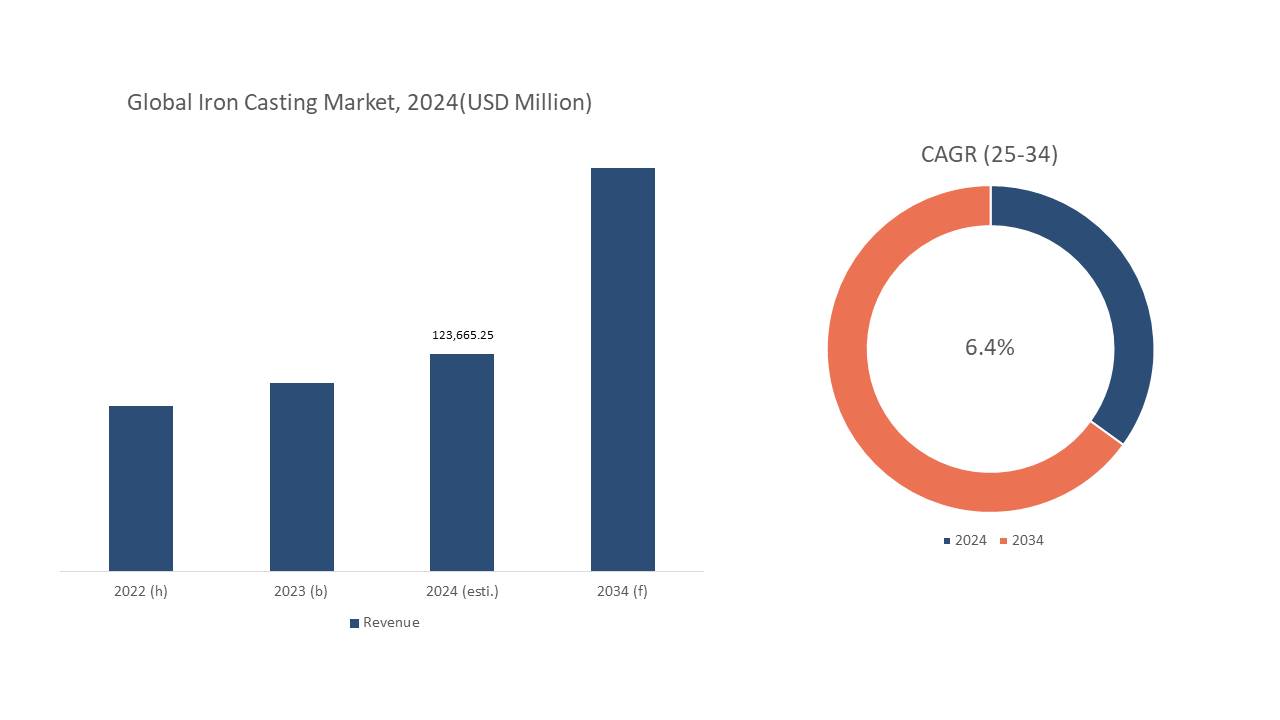

According to Novatrends Market Intelligence, the global iron casting market is valued at USD 123,665.2 million in 2024.Governments worldwide are pouring resources into infrastructure projects, including railways, bridges, and power grids. Iron castings, with their exceptional strength and durability, are ideal for these applications, fueling demand for pipes, fittings, and structural components. The rapid infrastructure development in countries like China and India is a major driver. These regions require cost-effective and robust solutions, making iron castings a prime choice.

The manufacturing sector, particularly in automobiles, machinery, and tools, is a significant consumer of iron castings. Their ability to withstand high pressures, abrasion, and stress makes them perfect for engine blocks, gears, and various equipment components.

Iron Casting Market Recent Developments

The iron casting market is anticipated to propel at a compounded annual growth rate (CAGR) of 6.4% from 2025-2032. The growing focus on renewable energy sources like wind and solar is creating demand for iron castings in turbines, generators, and other supporting structures.

The iron casting market is highly competitive due to the presence of major market players actively engaged in implementing strategic initiatives such as increasing investments, production expansion, enlarging distribution networks, and others. For instance,

- In June 2024, Casting PLC, an iron casting and machining group, announced the acquisition of fixed assets and stock of a Chamberlin subsidiary, namely, Russell Ductile Castings.

- In February 2024, Skuld LLC, an innovative iron casting company from the U.S., announced the expansion of their iron cast facility with the opening of a new foundry and manufacturing facility.

- In May 2024, MacLean Power Systems (MPS), a manufacturer of engineered products for transmission, distribution, substation, and communication infrastructure, announced the acquisition of Dotson Iron Castings.

Regional Overview

Asia Pacific dominated the global iron casting market in 2024 with a market revenue share of 37.32%. Asia Pacific is a manufacturing powerhouse for automobiles, machinery, and various industrial equipment. Iron castings, with their exceptional strength and machinability, are ideal for engine blocks, gears, and machine components, fueling demand across the region.

The rise of domestic consumption in countries such as China and India strengthen the demand for iron castings. As these economies grow, the need for local production of machinery and equipment increases, further driving the iron casting industry. Several Asian governments are promoting domestic manufacturing and reducing reliance on imports. This incentivizes the growth of the iron casting industry, creating a self-sufficient ecosystem.

U.S. Iron Casting Market Overview

The U.S. dominates the North American iron casting market due to a well-established manufacturing ecosystem and robust demand from key end-user segments. Major automotive OEMs (Original Equipment Manufacturers) and machinery & tool producers within the U.S. drive significant demand for iron castings.

Additionally, the expanding petrochemical industry necessitates a growing supply of pipes and fittings, further fueling market growth. Furthermore, ongoing infrastructure development projects across the country present a substantial opportunity for the iron casting industry.A major driver of the Iron Casting boom is the resurgence of the U.S. construction industry. According to the U.S. Census Bureau confirms the total construction spending (residential and non-residential) is expected to experience a surge of 3.5% year-over-year in June 2024. This growth across various construction segments is significantly boosting the demand for iron castings.

The demand for iron castings in the U.S. is projected to maintain a healthy growth trajectory in the coming years. Buoyed by the factors mentioned above, iron castings are well-positioned to take a dominant role in the U.S. construction materials market, catering to the needs of a resurgent construction industry and evolving environmental considerations.

Product Overview

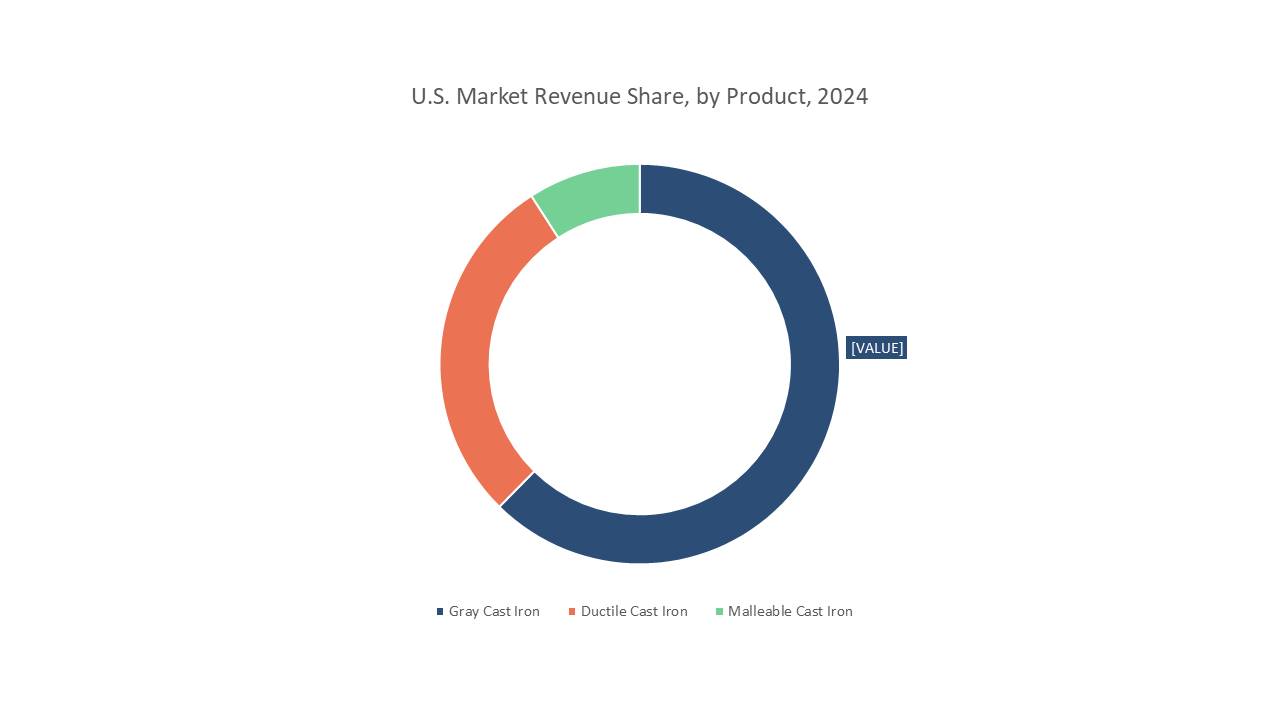

The gray cast iron dominated the application segmentation across the global iron casting market in 2024 with a market revenue share of 62.38%. Gray cast iron offers an exceptional balance between affordability, machinability, and good mechanical properties like strength and wear resistance. In applications where weight isn't a critical concern, its cost-effectiveness makes it a compelling choice.

The Iron Casting market is experiencing a growth surge, fueled by a rising demand from various construction sectors. While metal buildings remain a dominant application, a new player is emerging on the scene: post-frame buildings. This report delves into the rise of post-frame construction and its impact on the Iron Casting market.

Application Overview

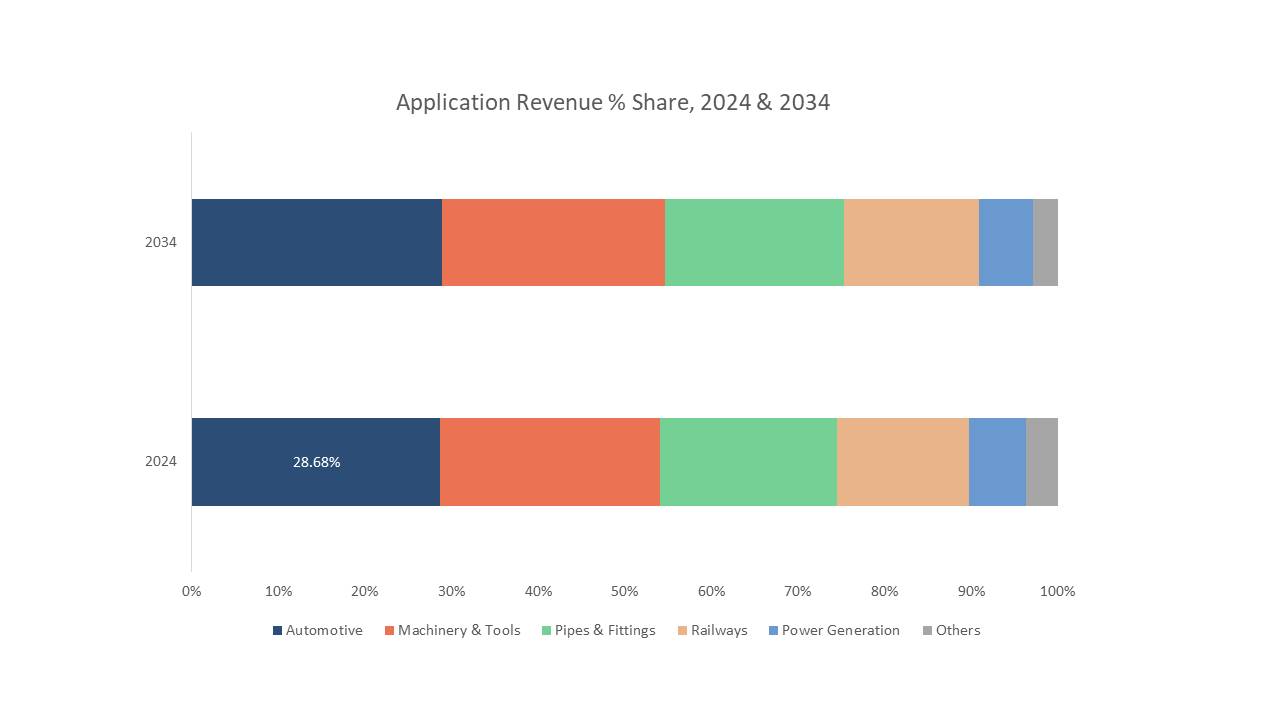

Automotive dominated the application segmentation across the global iron casting market in 2024 with a market revenue share of 28.68%. Despite advancements in lightweight materials, iron castings are experiencing a resurgence in the automotive industry. While lighter materials offer weight advantages, iron castings remain cost-effective for components where weight isn't a critical factor. Their affordability makes them a compelling choice for applications prioritizing strength, durability, and value.

The Iron Casting market is experiencing a growth surge, fueled by a rising demand from various construction sectors. While metal buildings remain a dominant application, a new player is emerging on the scene: post-frame buildings. This report delves into the rise of post-frame construction and its impact on the Iron Casting market.

Market Characteristics

The iron cast market is a dynamic and competitive arena, characterized by a diverse range of players and evolving market forces. The iron cast market is dominated by a large number of small and medium-sized foundries, particularly in developing regions. This creates a highly fragmented landscape with intense competition on price and production capacity.

However, recent years have witnessed a trend towards consolidation, with larger players acquiring smaller foundries to expand their geographical reach, product portfolio, and market share. Asia Pacific, led by China and India, is the undisputed leader in iron casting production and consumption due to its booming manufacturing sector and infrastructure development projects.

Developed economies such as North America and Europe are experiencing a shift towards high-value and specialized castings due to rising production costs and competition from emerging economies. For many players, particularly in price-sensitive markets, cost leadership remains a key strategy. This involves optimizing production processes, utilizing cost-effective raw materials, and focusing on high-volume production.

Global Iron Casting Market Report- Scope (Customizable)

|

Scope |

Description |

|

Historic Period |

2018-2032 |

|

Base Year (Esti.) |

2024 |

|

Forecast Period (F) |

2025-2032 |

|

Market Volume |

Kilotons |

|

Market Revenue |

USD Million |

|

Market by Product |

Gray Cast Iron, Ductile Cast Iron, and Malleable Cast Iron |

|

Market by Application |

Automotive, Machinery & Tools, Pipes & Fittings, Railways, Power Generation, and Others |

|

Market By Region |

North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

|

Countries Covered |

U.S., Canada, Mexico; Germany, UK, Italy, France, Spain, Russia; China, India, Japan, South Korea, Malaysia, Singapore, Thailand, Vietnam, Australia & New Zealand; Brazil, Argentina; Saudi Arabia, United Arab Emirates (UAE), Iran, South Africa |

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?