Market Overview

According to Novatrends Market Intelligence, the Global Geomembrane Market was valued at USD 3.8 billion in 2025 and is anticipated to propel at a growth rate of 6.4% from 2026-2036.

Geomembranes are low-permeability synthetic membrane liners used for fluid containment and environmental protection across numerous infrastructure and industrial applications. HDPE geomembrane liner systems are the dominant product type due to their superior geomembrane chemical resistance, geomembrane UV resistance properties, and long service life in geomembrane for landfill lining and geomembrane for mining applications. LLDPE geomembrane products offer superior flexibility and elongation for irregular surface geomembrane installation services, while PVC geomembrane liner solutions and textured geomembrane liner systems serve civil engineering and geomembrane for canal lining applications. Geomembrane pond liner systems and geomembrane for water containment in reservoirs and irrigation ponds are growing segments alongside geomembrane for agriculture irrigation in arid regions. Geomembrane for tailings dams in mining operations is a critical application requiring certified geomembrane quality testing standards and geomembrane welding technology expertise.

Market Dynamics

The market is driven by expanding global waste management infrastructure requiring geomembrane for landfill lining, growing mining sector investment in geomembrane for tailings dams and heap leach pads, and rising water scarcity concerns driving geomembrane for water containment and geomembrane for canal lining investment. Reinforced geomembrane products are gaining adoption in high-stress geomembrane for tunnel waterproofing applications, while sustainable geomembrane solutions with recycled content are emerging. Geomembrane welding technology advancement — including hot wedge and extrusion welding — is improving installation quality and geomembrane quality testing standards compliance. In February 2024, GSE Environmental expanded HDPE geomembrane liner systems production for North American landfill and mining markets, while AGRU Austria introduced sustainable geomembrane solutions with reduced carbon footprint for European environmental protection applications. Growing geomembrane for agriculture irrigation adoption in water-stressed regions and geomembrane installation services market professionalization are supporting robust market expansion through 2036.

Segment Analysis

By Material: HDPE holds the largest share of the Geomembrane market, supported by strong adoption and well-established supply chains across key end-use industries. LLDPE is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Application: Waste Management holds the largest share of the Geomembrane market, supported by strong adoption and well-established supply chains across key end-use industries. Mining is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By End-Use Industry: Environmental holds the largest share of the Geomembrane market, supported by strong adoption and well-established supply chains across key end-use industries. Mining is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

Recent Developments in Geomembrane Market

- In January 2024, GSE Environmental expanded HDPE geomembrane liner systems and textured geomembrane liner systems production for North American geomembrane for landfill lining and geomembrane for mining applications, reinforcing its leadership in geomembrane quality testing standards and geomembrane installation services.

- In April 2024, AGRU Austria introduced sustainable geomembrane solutions with recycled polymer content for European geomembrane environmental protection applications, meeting stringent geomembrane quality testing standards while reducing lifecycle carbon footprint of geomembrane for water containment projects.

- In July 2024, Solmax International launched reinforced geomembrane products for high-load geomembrane for tailings dams in South American and Australian mining operations, featuring advanced geomembrane chemical resistance and geomembrane welding technology for challenging site conditions.

- In October 2024, Officine Maccaferri expanded geomembrane for tunnel waterproofing and geomembrane for canal lining product lines for Middle East and North Africa water infrastructure projects, using PVC geomembrane liner solutions and LLDPE geomembrane products with proven geomembrane UV resistance properties.

- In January 2025, Firestone Building Products introduced EPDM geomembrane pond liner systems and geomembrane for agriculture irrigation products for U.S. water storage and irrigation applications, targeting sustainable geomembrane solutions for arid-region agricultural water efficiency programs.

- In March 2025, Atarfil (TenCate Geosynthetics) launched enhanced geomembrane installation services with digital geomembrane welding technology monitoring for geomembrane for mining applications and geomembrane for landfill lining projects requiring real-time geomembrane quality testing standards compliance.

Top Geomembrane Market - Key Market Players

- GSE Environmental

- AGRU Austria

- Solmax International

- Officine Maccaferri

- Firestone Building Products

- TenCate Geosynthetics (Atarfil)

- Layfield Group Ltd.

- Nilex Inc.

- Membrane International Inc.

- BTL Liners

- Canadian Geomembrane

- NAUE GmbH & Co. KG

- Raven Industries

- Geo-Synthetics Systems Inc.

- Hydrological Solutions Inc.

Global Geomembrane Market Report- Scope (Customizable)

Scope | Description |

Historic Period | 2021-2024 |

Base Year (Esti.) | 2025 |

Forecast Period (F) | 2026-2036 |

Market Values | USD Billion |

By Material | HDPE, LLDPE, PVC, EPDM, PP, Others |

By Application | Waste Management, Mining, Water Management, Agriculture, Oil & Gas |

By End-Use Industry | Environmental, Mining, Civil Engineering, Agriculture |

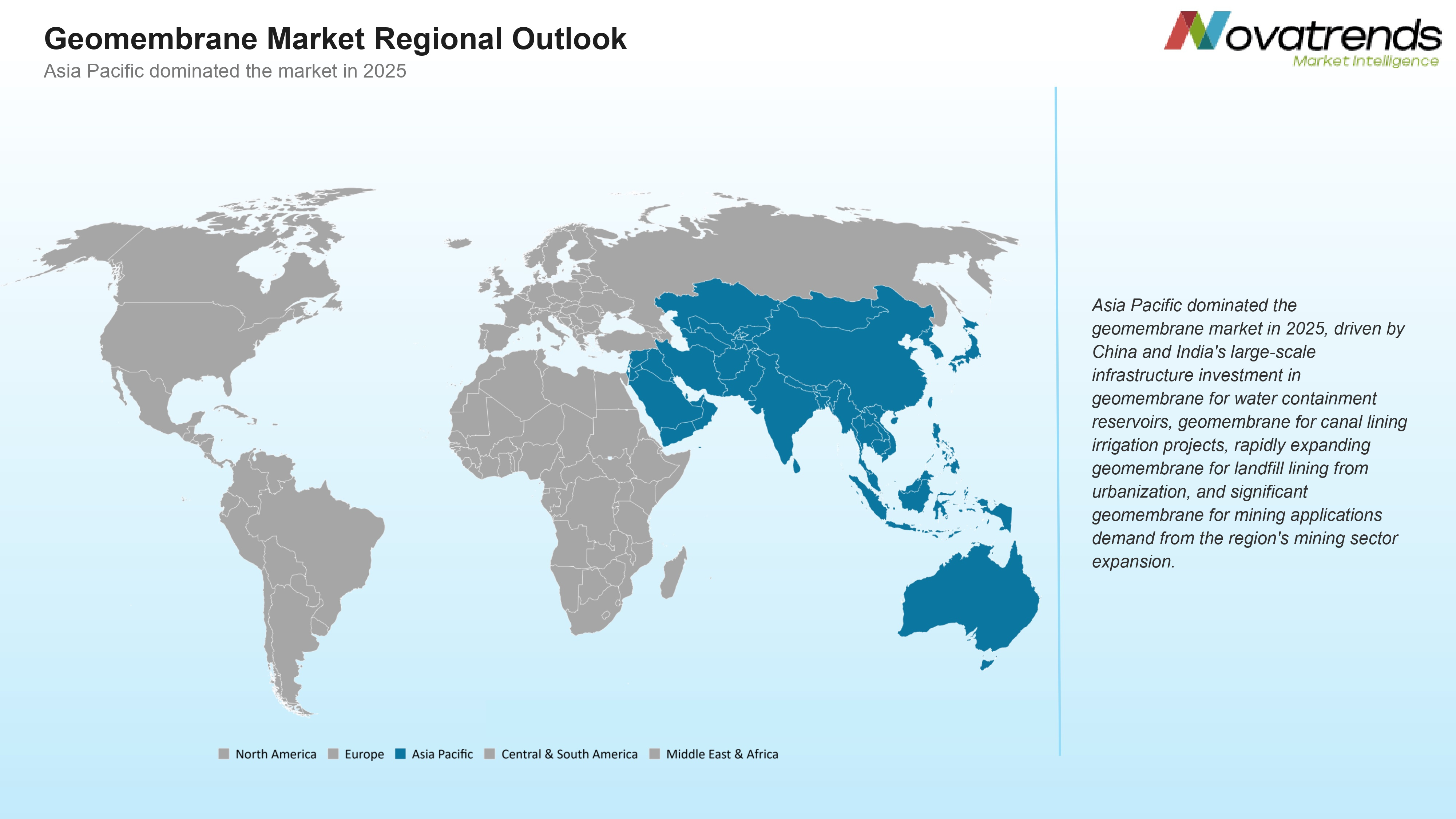

Market by Region | North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

Countries Covered | U.S., Canada, and Mexico; Germany, France, UK, Russia, Italy, Spain, and Netherlands; China, India, Japan, South Korea, and Australia; Brazil, Argentina; Saudi Arabia, UAE, Turkey, Egypt, and South Africa |

Detailed Market Segmentation

- By Material (Revenue in USD Million)

- HDPE

- LLDPE

- PVC

- EPDM

- PP

- Others

- By Application (Revenue in USD Million)

- Waste Management

- Mining

- Water Management

- Agriculture

- Oil & Gas

- By End-Use Industry (Revenue in USD Million)

- Environmental

- Mining

- Civil Engineering

- Agriculture

- By Region (Revenue in USD Million)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Russia

- Italy

- Spain

- Netherlands

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Central & South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Egypt

- South Africa

- North America

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?