Food Packaging Market Report Overview

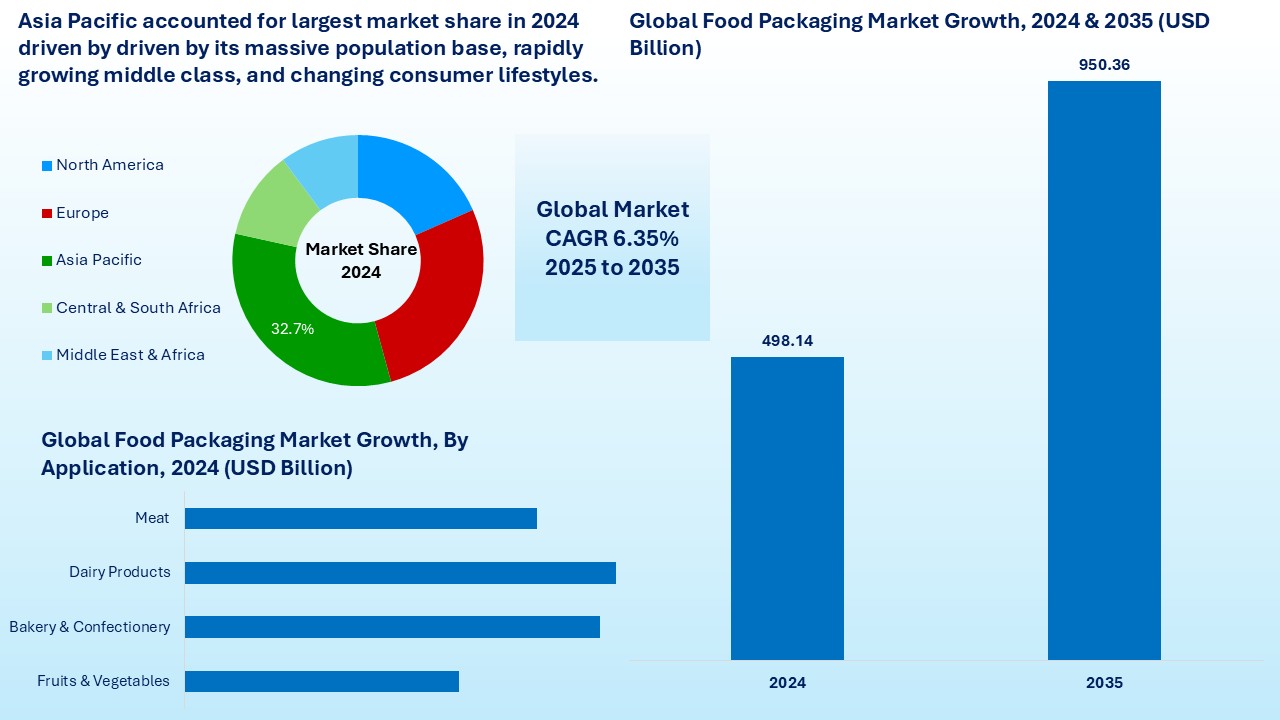

According to Novatrends Market Intelligence, the global Food Packaging market is valued at USD 498.14 billion in 2024. The global food packaging market is witnessing significant growth, driven by increasing demand for convenience, hygiene, and sustainability in food consumption. Rapid urbanization, rising disposable incomes, and changing consumer lifestyles are fueling the need for packaged and ready-to-eat foods. As a result, manufacturers are focusing on innovative packaging solutions that not only preserve food quality and extend shelf life but also cater to the growing preference for eco-friendly materials.

Sustainability has become a key focus, with companies adopting biodegradable, compostable, and recyclable packaging materials to reduce environmental impact and comply with stringent regulations. Plastic alternatives, such as paper, cardboard, and plant-based materials, are gaining popularity among consumers and brands alike. Additionally, technological advancements in smart packaging, such as QR codes and sensors that monitor freshness and temperature, are enhancing food safety and traceability across the supply chain. The rise of e-commerce and food delivery services is also creating new opportunities, increasing the demand for durable and tamper-proof packaging. With growing awareness of health, environmental, and safety concerns, the food packaging industry continues to evolve, offering innovative solutions that balance functionality, sustainability, and consumer appeal. This makes food packaging a crucial and dynamic part of the modern food ecosystem.

Industry Snapshot

Market Driver: Rise in E-commerce and Food Delivery → Increased Demand for Durable and Functional Packaging

The rapid growth of e-commerce platforms and food delivery services has significantly influenced the food packaging market. As consumers increasingly opt for online grocery shopping and home-delivered meals, packaging must adapt to ensure food safety, temperature control, and tamper resistance. This shift has created a strong need for packaging that can withstand transit conditions without compromising product quality.

The increase in cloud kitchens and quick-service restaurants has further accelerated this trend. Packaging is now expected to offer durability, insulation, and leak-proof features, along with attractive branding to enhance customer experience. As a result, companies are investing in high-performance packaging solutions like multi-layer films, insulated containers, and moisture-resistant wraps.

This demand is also driving innovation in sustainable yet sturdy materials that serve both environmental and functional goals. The direct effect is a surge in packaging technology development, pushing the market forward and creating a competitive edge for manufacturers who deliver on quality and design.

Market Restraint: Environmental Regulations and Plastic Waste → Pressure to Transition to Sustainable Alternatives

The widespread use of single-use plastic in food packaging has led to serious environmental concerns, prompting governments and regulatory bodies worldwide to impose strict regulations. Bans on certain types of plastic packaging, mandatory recycling norms, and extended producer responsibility (EPR) schemes are putting increased pressure on food packaging manufacturers to shift toward sustainable materials. This regulatory push has forced companies to invest in research and adopt eco-friendly alternatives such as biodegradable plastics, paper-based packaging, and reusable materials. However, these sustainable solutions often come with higher production costs, limited availability, and technical challenges like reduced barrier properties or shorter shelf life.For many small and medium-sized enterprises, the cost and complexity of compliance can be a significant burden, resulting in reduced margins or inability to scale. In some cases, lack of infrastructure for recycling and composting adds further complications, undermining the effectiveness of these green initiatives.

Thus, while these regulations are environmentally necessary, they act as a restraint on the food packaging market by increasing operational costs, complicating production processes, and limiting material choices, especially for companies in cost-sensitive or developing regions.

Market Opportunity: Growing Demand for Sustainable Packaging → Innovation in Eco-friendly Materials

As environmental awareness rises among consumers, there is a growing demand for food packaging that is biodegradable, recyclable, compostable, or reusable. This shift in consumer preference is creating a major opportunity for companies to innovate and offer packaging solutions that align with sustainability goals.

Brands are now actively seeking packaging that reduces carbon footprint without compromising food safety, shelf life, or visual appeal. This demand has spurred research into alternative materials such as plant-based plastics (PLA), molded fiber, edible films, and recycled paperboard. Companies that invest early in scalable, sustainable technologies are well-positioned to lead the market. Retailers and foodservice providers are also adopting eco-friendly packaging as part of their ESG (Environmental, Social, and Governance) commitments, boosting demand across the supply chain. Moreover, consumers are increasingly rewarding brands that demonstrate genuine environmental responsibility, translating into stronger customer loyalty and improved brand image.

This opportunity enables businesses to differentiate themselves through innovation while also meeting regulatory requirements and ethical expectations. As a result, the push for sustainable food packaging is not only a moral and legal imperative but also a lucrative avenue for growth, particularly in markets where environmental concerns influence purchasing decisions.

Segmental Overview

By Material

Based on Material, Food Packaging Market is segmented into Glass, Metal, Paper & Paperboard, and wood. Plastics is expected to dominate the market in 2024 owing the increasing demand for biodegradable packaging across globe. One of the primary drivers of the plastic packaging market is the strong demand for lightweight, durable, and cost-effective packaging solutions across industries—especially in food and beverages, pharmaceuticals, and personal care. Plastic packaging offers exceptional versatility, allowing manufacturers to mold it into various shapes, sizes, and functional designs to suit a wide range of products.

Glass, metal, paper, and paperboard packaging each offer distinct benefits and serve specific needs across the packaging industry. Glass packaging is valued for its non-reactive, premium, and reusable nature, making it ideal for beverages, pharmaceuticals, and high-end food products. Metal packaging, commonly in the form of aluminum and steel, provides excellent barrier protection, durability, and recyclability, widely used in canned foods, aerosols, and beverages. Paper and paperboard packaging are favored for their biodegradability, printability, and cost-effectiveness, commonly used in cartons, boxes, and bags across food, retail, and e-commerce. Together, these materials offer a mix of sustainability, functionality, and branding flexibility, catering to diverse consumer and regulatory demands.

By Product Type

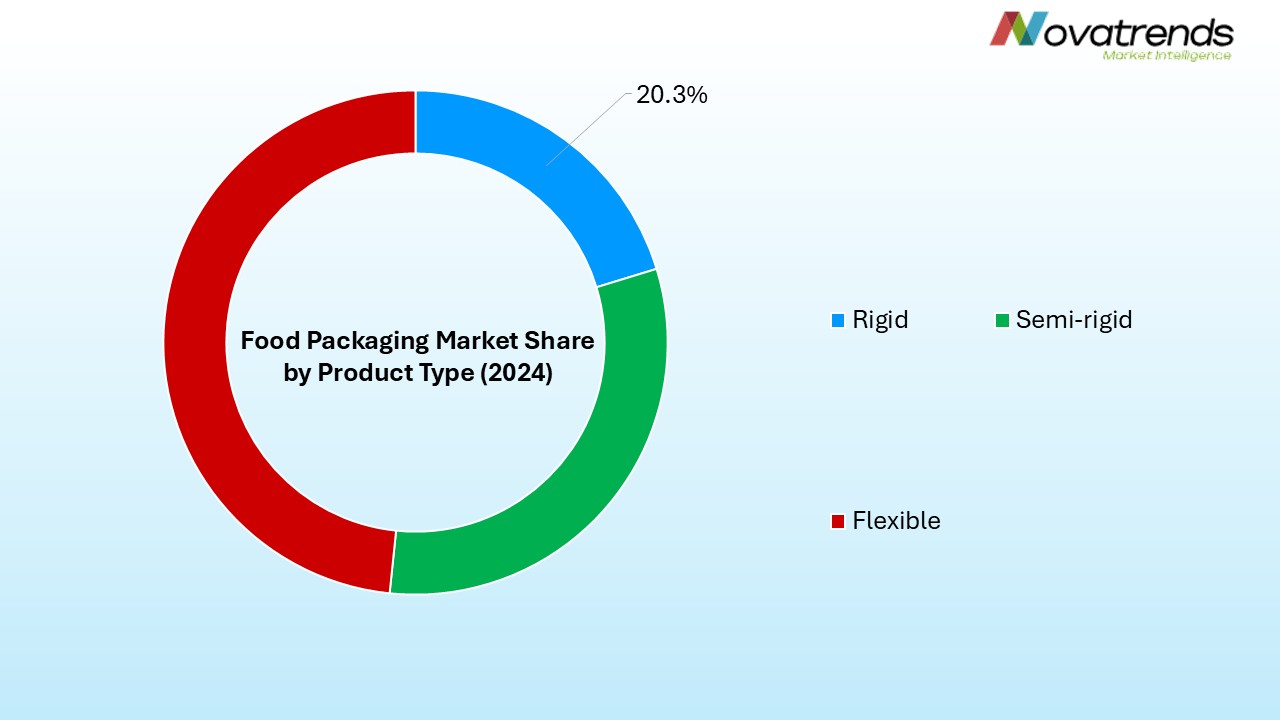

Based on Product Type, Food Packaging Market is segmented into Rigid, Semi-rigid, and Flexible. The food packaging market is segmented into rigid, semi-rigid, and flexible packaging types, each catering to different product needs and consumer preferences. Among these, rigid packaging currently dominates the market due to its superior protection, durability, and suitability for a wide range of food products. Rigid packaging materials, such as glass jars, metal cans, and hard plastic containers, provide excellent barrier properties against moisture, oxygen, and contaminants, which helps preserve food quality and extends shelf life. Additionally, rigid packaging supports easy stacking and transportation, making it a preferred choice for bulk and premium food items, including dairy, beverages, canned goods, and frozen foods. The established infrastructure for producing and recycling rigid packaging further supports its market dominance.

On the other hand, the fastest-growing segment is flexible packaging, driven by evolving consumer demands for convenience, sustainability, and cost-efficiency. Flexible packaging, which includes pouches, bags, wraps, and films, offers lightweight, space-saving, and versatile solutions that significantly reduce material usage and transportation costs. This type of packaging is highly adaptable, able to accommodate various product shapes and sizes while providing excellent sealing capabilities and barrier protection. Innovations such as resealable zippers, spouts, and printable surfaces enhance user experience and brand visibility. Moreover, flexible packaging aligns well with the growing trend towards on-the-go consumption, portion control, and sustainable packaging alternatives, including recyclable and biodegradable films. Semi-rigid packaging, which bridges the gap between rigid and flexible types, is also gaining traction but at a slower pace compared to flexible packaging. Overall, while rigid packaging remains the market leader due to its robustness and protection, flexible packaging’s rapid adoption is reshaping the industry landscape by addressing modern consumer needs and environmental concerns, making it the fastest-growing segment globally.

By Application

Based on Application, the food packaging market segmented by application into Fruits & Vegetables, Bakery & Confectionery, Dairy Products, Meat, Poultry & Seafood, and Sauces, Dressings & Condiments reflects varied demand driven by consumer habits and product characteristics. Among these, the Dairy Products segment is expected to dominate the market. This dominance is largely due to the high consumption of dairy worldwide and the stringent packaging requirements to maintain product freshness, extend shelf life, and ensure safety. Dairy products such as milk, cheese, yogurt, and butter are highly perishable and require packaging with excellent barrier properties against oxygen, moisture, and light to prevent spoilage. Moreover, innovations like resealable containers, portion packs, and eco-friendly packaging in this segment enhance convenience and sustainability, further solidifying its leading position.

In contrast, the fastest-growing segment is likely to be Fruits & Vegetables packaging. The surge in health-conscious consumer behavior globally has increased demand for fresh produce consumption, both raw and minimally processed. This shift fuels the need for packaging that can preserve freshness, reduce waste, and provide convenience—such as breathable films, modified atmosphere packaging (MAP), and biodegradable bags. Additionally, the rise of online grocery shopping has intensified demand for durable, protective packaging to ensure fruits and vegetables reach consumers in optimal condition. Growing urbanization and changing lifestyles, particularly in emerging markets, also contribute to the rapid growth of this segment.

Other segments like Bakery & Confectionery and Meat, Poultry & Seafood are growing steadily but face challenges related to hygiene and shelf life, while Sauces and Dressings benefit from niche growth in convenience and single-serve packaging. Overall, dairy remains dominant due to volume and packaging complexity, while fruits and vegetables lead growth driven by health trends and fresh food demand.

By Packaging Type

Based on Packaging Type, the food packaging market segmented into Bags & Pouches, Films & Wraps, Stick Packs & Sachets, Bottles & Jars, Boxes & Cartons, Cans, Trays, & Clamshells reflects the diverse packaging needs across the food industry. Among these, Bags & Pouches are expected to dominate the market due to their versatility, cost-effectiveness, and convenience. Bags and pouches are widely used for a variety of food products such as snacks, frozen foods, pet food, and powdered items. Their lightweight nature reduces transportation costs and carbon footprint, while advancements like resealable zippers and spouts enhance user convenience. Additionally, bags and pouches require less material compared to rigid packaging, aligning with growing sustainability concerns. Their ability to incorporate multiple layers for barrier protection makes them ideal for preserving freshness and extending shelf life, driving their widespread adoption.

Meanwhile, the fastest-growing segment is likely to be Films & Wraps. Flexible films and wraps are increasingly popular due to their adaptability, minimal material usage, and ability to provide effective protection for fresh produce, bakery items, and ready-to-eat meals. Innovations such as biodegradable and compostable films are meeting rising consumer and regulatory demands for sustainable packaging options. The surge in online grocery shopping and home food delivery also drives demand for flexible films that can securely wrap and protect food during transit while offering convenience and visibility. Films and wraps provide excellent customization opportunities for branding and product information, further boosting their market growth.

Other packaging types like bottles, jars, and cans continue to be important for beverages and preserved foods, while boxes, cartons, trays, and clamshells serve niche markets needing rigid protection. However, bags and pouches dominate due to their balance of cost, performance, and sustainability, while films and wraps grow fastest, fueled by innovation and changing consumer lifestyle.

By End-User

Based on End-User, the food packaging market segmented by end-users into Quick Service Restaurants (QSRs), Full Service Restaurants (FSRs), Cafes & Kiosks, and Chain Restaurants shows varying demand driven by consumer dining habits and industry dynamics. Among these, Quick Service Restaurants (QSRs) are expected to dominate the market due to their widespread global presence and the growing preference for fast, convenient, and affordable food options. QSRs heavily rely on packaging for takeout and delivery services, which has surged with the rise of online food delivery platforms and changing consumer lifestyles. Packaging for QSRs emphasizes portability, food safety, and branding, with materials designed to keep food warm, fresh, and spill-proof. The high volume of transactions in QSRs and their continuous expansion, especially in urban and emerging markets, contribute significantly to the demand for innovative and cost-effective packaging solutions, ensuring QSRs remain the largest segment.

Conversely, the fastest-growing segment is likely to be Cafes & Kiosks, driven by the increasing popularity of on-the-go food and beverages such as coffee, snacks, and quick bites. As consumer lifestyles become busier, cafes and kiosks are expanding in both urban and suburban areas, offering convenient, small-portion, and takeaway-friendly food options. Packaging innovations in this segment focus on sustainability, lightweight materials, and convenience features like resealable lids and eco-friendly cups, which appeal strongly to environmentally conscious consumers. Additionally, cafes and kiosks often target younger demographics who value aesthetics and brand experience, pushing demand for visually appealing and functional packaging.

Full Service and Chain Restaurants maintain steady growth but typically rely more on dine-in service with less frequent packaging usage for takeout compared to QSRs and cafes. Overall, QSRs dominate due to volume and convenience demand, while cafes and kiosks grow fastest, fueled by lifestyle trends and sustainability concerns.

Regional Overview

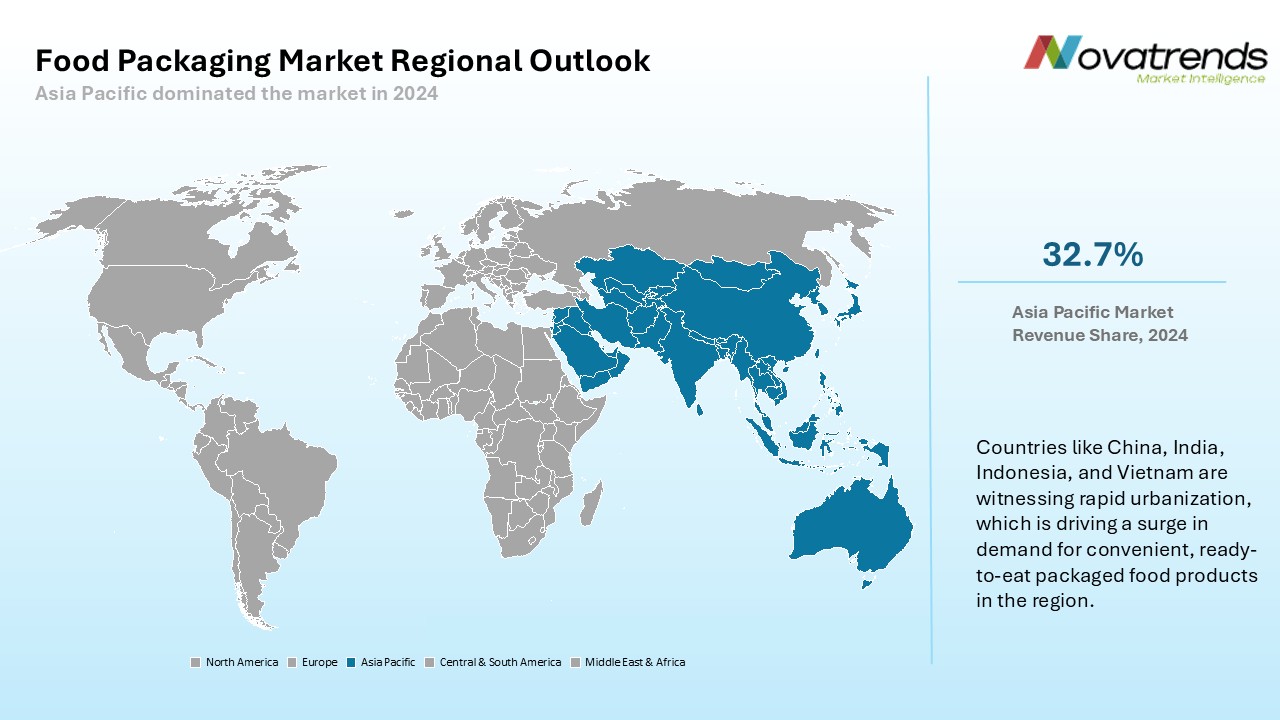

Asia Pacific dominated the global Food Packaging market in 2024 with a market share. Food Packaging demand in the Asia Pacific region has surged due to a combination of factors. Increasing geopolitical tensions and territorial disputes have prompted substantial defense spending, driving up Food Packaging purchases. The region's economic growth has led to higher disposable incomes, fueling civilian demand for Food Packaging.

Additionally, population growth and urbanization have contributed to the overall increase in Food Packaging consumption. The prevalence of natural disasters and the growing arms trade within the region further amplify this trend. Each country within the region exhibits unique dynamics influenced by specific factors, such as India's focus on internal security and defense modernization, or South Korea and Taiwan's emphasis on deterrence.

North America

The North American food packaging market is mature and highly developed, driven by strong demand for convenience foods, stringent food safety regulations, and growing adoption of sustainable packaging solutions. The region’s consumers prioritize health, hygiene, and eco-friendly packaging, pushing innovations in biodegradable materials and recyclable plastics. The rise of e-commerce and food delivery services has further accelerated demand for flexible and functional packaging. The United States and Canada lead the market, supported by advanced manufacturing infrastructure and regulatory frameworks encouraging sustainability.

Europe

Europe is a key market with a strong focus on sustainability and environmental regulations. Strict government policies on plastic reduction and waste management are encouraging the shift towards biodegradable, recyclable, and reusable packaging. Countries like Germany, France, and the UK are pioneers in adopting eco-friendly packaging technologies. The growing organic food segment and consumer awareness about health and environmental impacts are significant growth drivers. Europe also has a robust market for premium and innovative packaging solutions that improve shelf life and convenience.

Asia Pacific

Asia Pacific is the fastest-growing region in the food packaging market due to rapid urbanization, rising disposable incomes, and expanding organized retail sectors in countries like China, India, Japan, and Southeast Asia. Increasing demand for packaged convenience foods and ready-to-eat meals is driving growth. However, challenges like varying regulations and infrastructure gaps persist. The region is witnessing rising adoption of flexible packaging and sustainable alternatives, supported by government initiatives and consumer awareness.

Central & South America

The food packaging market in Central and South America is growing steadily, fueled by increasing food processing industries and expanding retail sectors in Brazil, Argentina, and Mexico. There is rising demand for affordable, protective packaging to reduce food spoilage amid supply chain challenges. However, sustainability adoption is slower compared to developed markets, mainly due to cost concerns and infrastructure limitations. Flexible and rigid packaging segments are growing as food consumption patterns evolve.

Middle East & Africa

The Middle East & Africa food packaging market is emerging, driven by urbanization, increasing food imports, and growth in fast food and convenience food sectors. Packaging innovations focus on enhancing shelf life and protecting against harsh climatic conditions. However, limited recycling infrastructure and high costs of sustainable materials slow the adoption of eco-friendly packaging. Countries like UAE, South Africa, and Saudi Arabia lead market development, with growing interest in modern retail formats and food safety compliance.

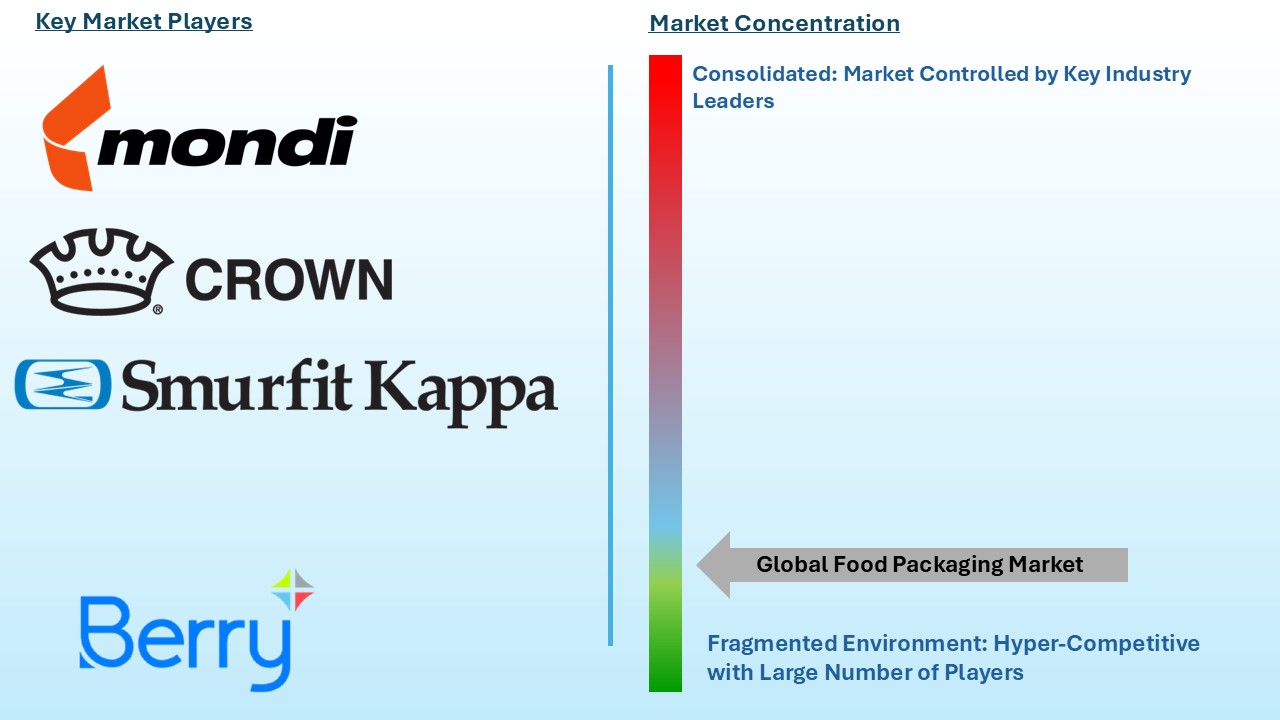

Competitive Landscape

The food packaging market is highly competitive and fragmented, with a mix of global conglomerates, regional manufacturers, and specialized niche players. Leading companies focus on innovation, sustainability, and expanding their product portfolios to meet evolving consumer demands and regulatory requirements. Key market participants include Amcor Limited, Sealed Air Corporation, Berry Global Inc., Tetra Pak International S.A., Mondi Group, Huhtamaki Oyj, Sonoco Products Company, and International Paper Company among others.

These companies compete primarily on the basis of product innovation, sustainability initiatives, pricing, quality, and global distribution networks. Innovation is centered around developing biodegradable, recyclable, and compostable packaging materials to address environmental concerns. For example, several players invest heavily in bio-based plastics, paper-based packaging, and multi-layer films with enhanced barrier properties.

Strategic mergers and acquisitions are common, allowing companies to strengthen market presence, expand geographic reach, and diversify product offerings. Collaborations with food manufacturers and retailers to co-develop customized packaging solutions are also a key trend, aimed at enhancing product differentiation and consumer appeal.

Moreover, companies increasingly adopt digital technologies like smart packaging (QR codes, freshness indicators) to improve consumer engagement and traceability. The competitive landscape is further shaped by regional dynamics—global players dominate in developed markets like North America and Europe, while regional and local manufacturers hold strong positions in emerging markets such as Asia Pacific, Latin America, and Africa.

Key Market Players

- Amcor plc

- Berry Global Group, Inc.

- Sealed Air Corporation

- Tetra Pak International

- Mondi Group

- Smurfit Kappa Group

- DS Smith

- Sonoco Products Company

- Huhtamäki Oyj

- Graphic Packaging International

- International Paper Company

- Ball Corporation

- Reynolds Group Holdings

- Crown Holdings, Inc.

- WestRock Company

Major Industry Updates

The food packaging industry is undergoing significant transformations driven by sustainability, technology, and regulatory changes. Key trends include the adoption of biodegradable materials like PHAs, the integration of smart packaging with QR codes and sensors for real-time freshness monitoring, and minimalist, functional designs. Events like FoodTech Kerala highlight innovations in eco-friendly packaging, while global shifts push for reduced plastic use and enhanced recycling efforts.

- In April 2025, ULMA Packaging has launched a new range of thermoforming machines tailored for the food packaging sector. This new line aims to enhance efficiency, sustainability, and packaging quality, integrating features such as improved sealing technologies, reduced material waste, and compatibility with recyclable or compostable films. The innovation aligns with market demand for eco-friendly and cost-effective solutions in food packaging.

- In March 2025, Borealis, in partnership with Ecoplast, has launched Borcycle M CWT120CL, a recycled linear low-density polyethylene (rLLDPE) containing 85% post-consumer recyclate. Designed for non-food flexible packaging, it offers superior stretchability, low gel content, and an ideal toughness-stiffness balance. This innovation underscores Borealis’ EverMinds™ initiative, promoting circularity and sustainability in plastic packaging through advanced recycling solutions.

- In February 2025, Berry Global and Mars introduced 100% recycled plastic pantry jars for M&M’S, SKITTLES, and STARBURST brands, excluding the lids. This initiative builds upon their 2022 launch, which featured jars with 15% recycled content. The new jars, available in 60-, 81-, and 87-ounce sizes, are crafted from certified food-grade, mechanically recycled PET sourced from curbside collections. This transition is expected to eliminate over 1,300 metric tons of virgin plastic annually, equivalent to the weight of approximately 238 African elephants. The jars are widely recyclable, supporting Mars' Sustainable Packaging Plan aimed at ensuring all packaging is reusable, recyclable, or compostable.

- In September 2024, Marigold Health Foods partnered with Sonoco to introduce fully recyclable packaging for its plant-based product range, including nutritional yeast, bouillon, sauces, and meat alternatives. The new EnviroCan features a can body made from 95% paper, with 60% sourced from post-consumer recycled fiber, and a 5% inner liner for product protection. This packaging is recyclable via the UK’s paper waste stream and displays the OPRL recycling logo to guide consumers.

Global Food Packaging Market Research Report- Scope (Customizable)

|

Scope |

Description |

|

Historic Period |

2018-2023 |

|

Base Year (Esti.) |

2024 |

|

Forecast Period (F) |

2025-2035 |

|

Market Revenue |

USD Billion |

|

Market by Material |

Glass, Metal, Paper & Paperboard, Plastic {Non-biodegradable, Biodegradable}, & Wood |

|

Market by Product Type |

Rigid, Semi-rigid, & Flexible |

|

Market by Application |

Fruits & Vegetables, Bakery & Confectionery, Dairy Products, Meat, Poultry & Seafood, Sauces, Dressings, & Condiments |

|

Market by Packaging Type |

Bags & Pouches, Films & Wraps, Stick Packs & Sachets, Bottles & Jars, Boxes & Cartons, Cans, Trays, & Clamshells |

|

Market by End-user |

Quick & Full Service Restaurants, Cafe & Kiosks, & Chain Restaurants and others |

|

Market By Region |

North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

|

Countries Covered |

U.S., Canada, Mexico; Germany, UK, Italy, France, Spain, Russia; China, India, Japan, South Korea, Malaysia, Singapore, Thailand, Vietnam, Australia & New Zealand; Brazil, Argentina; Saudi Arabia, United Arab Emirates (UAE), Iran, South Africa |

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?