Aviation Fuel Market Report Overview

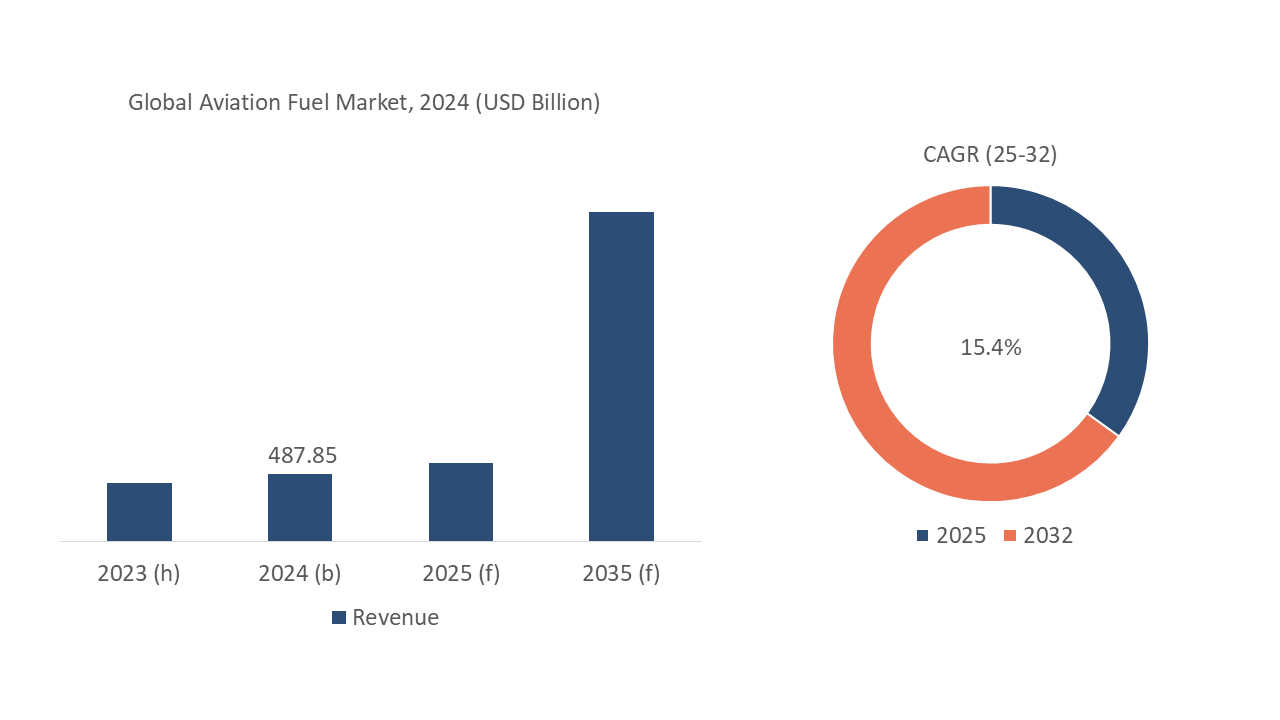

According to Novatrends Market Intelligence, the global aviation fuel market was valued at USD 487.85 million in 2024 and is anticipated to propel at a growth rate of 15.4% from 2025-2032.

The aviation fuel market is driven by several key factors that reflect both the growing demand for air travel and the industry's efforts toward sustainability. One of the primary drivers is the increasing global demand for air transportation, spurred by rising disposable incomes, rapid urbanization, and the growth of international trade and tourism. The proliferation of low-cost carriers and the expanding middle class, particularly in emerging markets such as Asia-Pacific, are further fueling this demand.

Moreover, the e-commerce boom has heightened the need for efficient cargo transport, adding pressure to the aviation sector's fuel requirements. However, this increasing demand is met with rising concerns about the environmental impact of aviation, leading to stringent regulations and carbon reduction goals set by governments and international organizations.

Governments around the world are offering incentives to promote SAF production and use, further boosting market growth. Lastly, geopolitical factors, such as trade policies, oil production levels, and global conflicts, continue to influence the stability and price of aviation fuel. Together, these factors create a dynamic and evolving landscape for the aviation fuel market, balancing growth in demand with the push for cleaner, more sustainable fuel solutions.

Aviation Fuel Market Recent Developments

Aviation Fuel Market is anticipated to propel at a compounded annual growth rate (CAGR) of 15.4% from 2025-2032. Recent developments in the aviation fuel market are largely centered around the growing emphasis on sustainability and the push for decarbonization. The adoption of sustainable aviation fuels (SAF) has accelerated, with airlines and fuel producers increasing investments in SAF production to meet stringent emissions reduction targets set by governments and international organizations. Several major airlines have committed to ambitious net-zero emissions goals, driving demand for SAF despite its higher cost and limited availability.

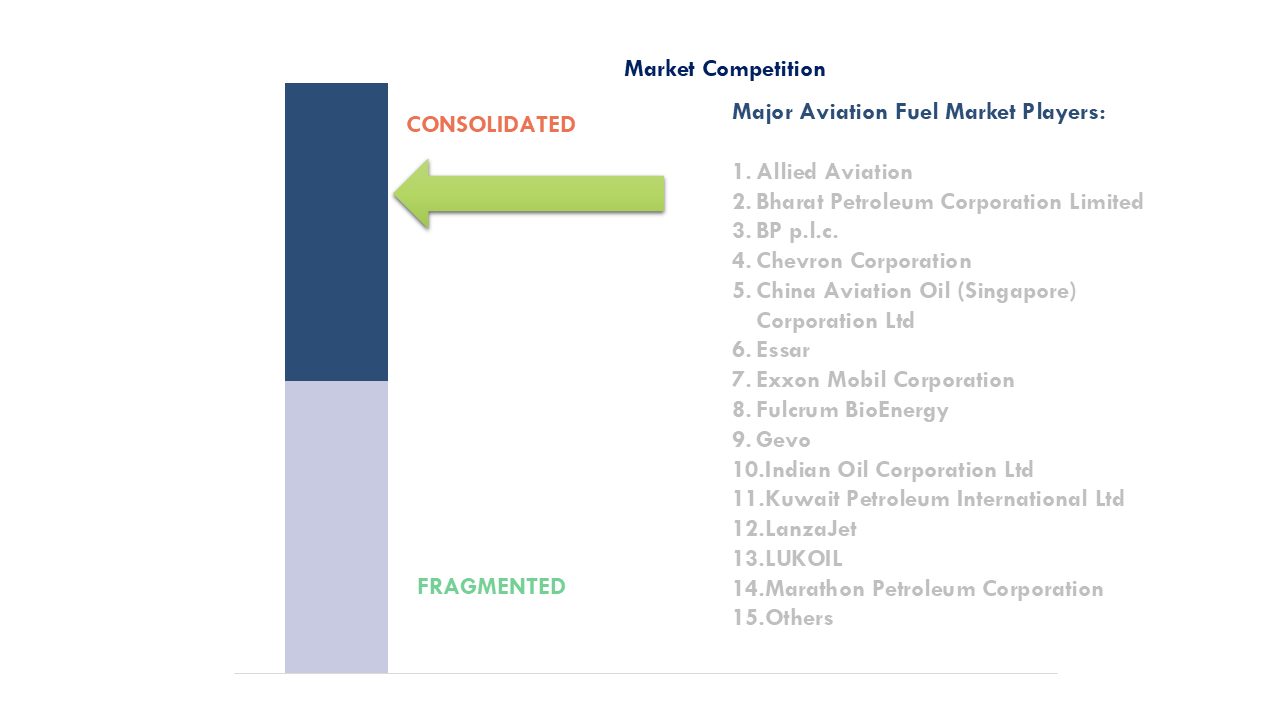

- In May 2024, Neste expanded its ability to supply sustainable aviation fuel (SAF) across Europe through a partnership with VTTI, a global leader in energy storage and infrastructure development. Neste has commissioned terminal capacity at VTTI’s ETT terminal in Rotterdam, Netherlands, to facilitate the storage and blending of Neste MY Sustainable Aviation Fuel. This collaboration strengthens Neste’s position in the European SAF market, enabling greater availability of sustainable fuel solutions for customers.

- In May 2024, LanzaJet announced a groundbreaking USD 20 million investment from global airport operator Groupe ADP. This investment in sustainable aviation fuel (SAF) technology and development will support LanzaJet's growth and enhance its crucial role within the SAF ecosystem.

- In April 2024, Boeing announced its largest purchase of blended sustainable aviation fuel (SAF) to date, acquiring 9.4 million gallons (35.6 million liters) to support its U.S. commercial operations in 2025. This significant purchase aims to reduce carbon emissions while contributing to the global expansion of SAF supply. The volume represents a more than 60% increase compared to the company’s SAF purchase in 2023.

- In September 2023, Airbus has partnered with DG Fuels to promote the production of sustainable aviation fuel (SAF) in the United States. This collaboration aims to scale up innovative technology that converts cellulosic waste and residues into sustainable aviation fuels.

Regional Overview

Asia Pacific dominated the global Aviation Fuel Market in 2024 with a market revenue share of 32.43%. The Asia-Pacific aviation fuel market is primarily driven by rapid economic growth, increasing urbanization, and rising disposable incomes across emerging markets like China, India, and Southeast Asia. This has led to a surge in both domestic and international air travel, with the region becoming a global hub for tourism and business travel.

The expansion of low-cost carriers (LCCs) has also made air travel more accessible to the growing middle class, further boosting demand for aviation fuel. Additionally, the rise of e-commerce and the associated need for efficient cargo transport have driven fuel consumption in the aviation sector.

However, the region faces increasing pressure to address environmental concerns, leading to the development and adoption of sustainable aviation fuels (SAF) to meet emissions reduction targets. Governments in Asia-Pacific are actively supporting SAF initiatives and encouraging investments in cleaner technologies through regulations and incentives. Fluctuations in crude oil prices and geopolitical factors also influence the market, impacting fuel costs and airline profitability. As Asia-Pacific continues to lead global aviation growth, balancing rising fuel demand with sustainability goals remains a key market driver.

U.S. Aviation Fuel Market Overview

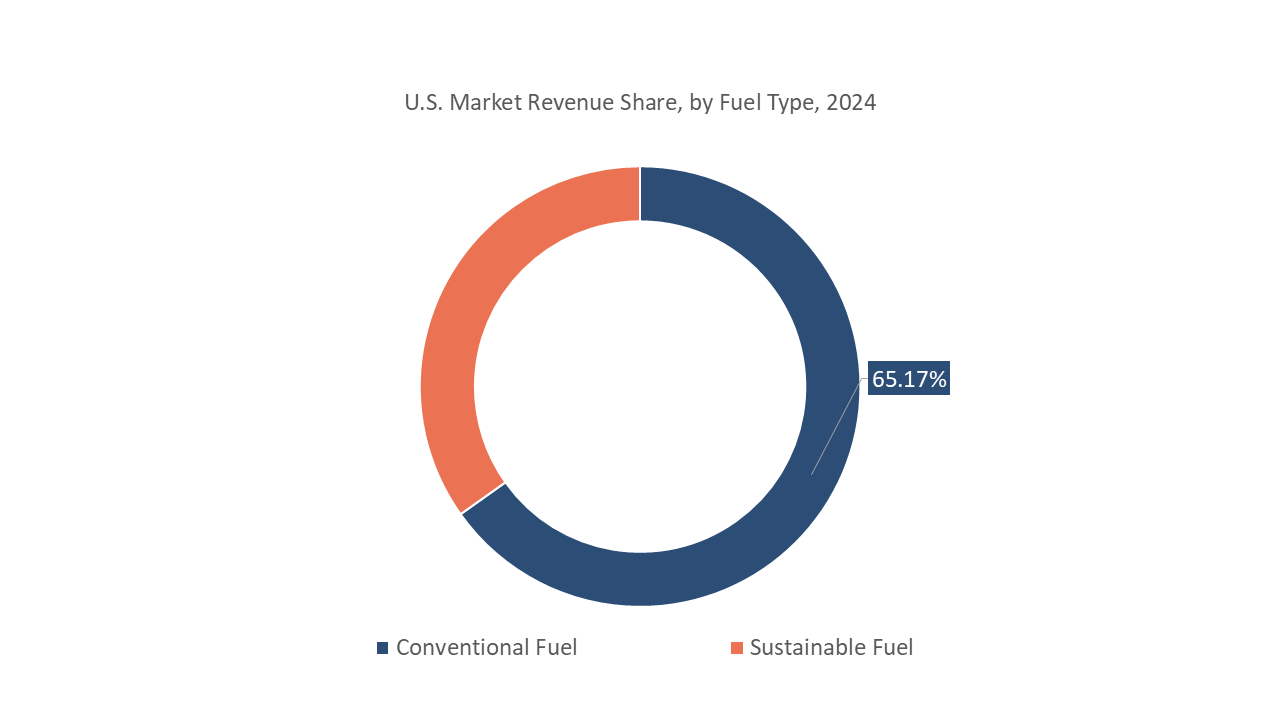

The U.S. aviation fuel market is driven by a high demand for both domestic and international air travel, bolstered by a robust economy, a well-established aviation infrastructure, and increasing e-commerce activities that require efficient cargo transport. The presence of major airlines and airports across the country supports strong fuel consumption. Environmental regulations and the push toward reducing carbon emissions are driving the development and adoption of sustainable aviation fuels (SAF), as airlines aim to meet carbon reduction targets. Additionally, government incentives and investments in SAF production are shaping the market.

In addition, advancements in fuel-efficient aircraft and engine technologies are playing a critical role in reducing fuel consumption per flight, creating a shift in demand patterns. The U.S. government’s role in promoting research and innovation in cleaner technologies, along with increasing investments in SAF infrastructure, is expected to significantly impact the long-term trajectory of the U.S. aviation fuel market, balancing the industry’s growth with sustainability goals.

Fuel Type Overview

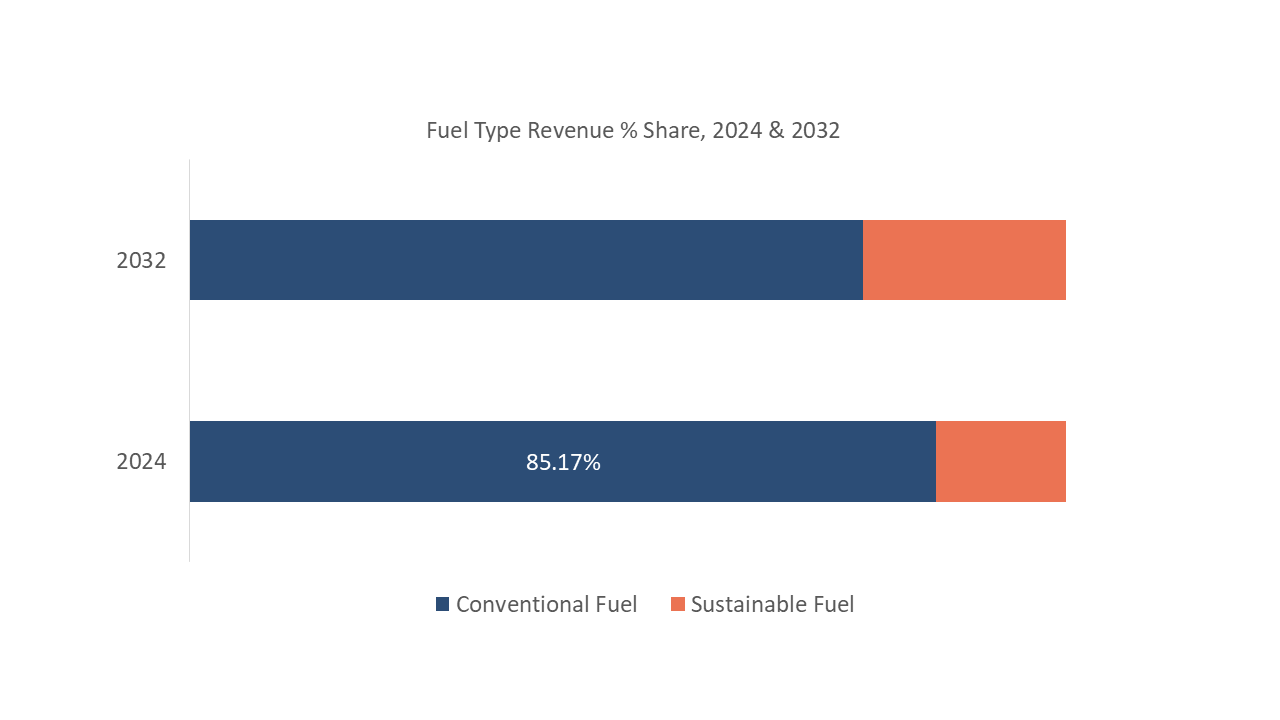

Conventional Fuel dominated the fuel type segmentation across the global aviation fuel market in 2024 with a market revenue share of 85.17%. The conventional aviation fuel market is driven by the continued dominance of fossil fuels in powering the global aviation industry, which remains heavily reliant on kerosene-based jet fuels like Jet-A and Jet-A1. Growing air travel demand, fueled by increased passenger traffic, global tourism, and expanding cargo transport, keeps the consumption of conventional fuels high. The availability of well-established infrastructure for fuel production, refining, and distribution also supports the widespread use of conventional aviation fuel.

However, fluctuations in crude oil prices directly impact costs and profitability for airlines. Despite increasing environmental regulations and the push for sustainable aviation fuels (SAF), conventional fuels continue to dominate due to their relatively lower cost, mature supply chains, and the gradual pace of SAF adoption. Technological advancements in fuel-efficient aircraft mitigate some fuel demand but don’t yet fully replace the need for conventional aviation fuels.

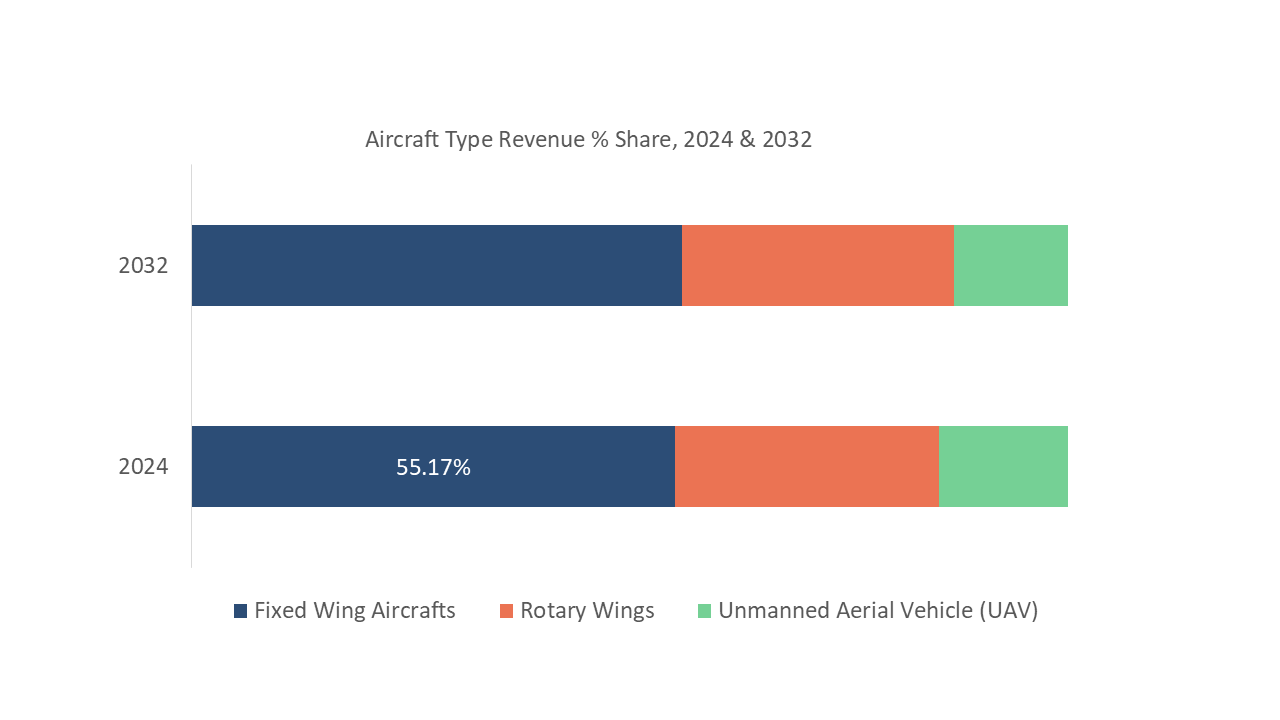

Aircraft Type Overview

Fixed Wing Aircrafts dominated the Aircraft Type segmentation across the global aviation fuel market in 2024 with a market revenue share of 55.17%. The aviation fuel market for fixed-wing aircraft is driven by the growing global demand for air travel, including commercial passenger flights, military operations, and cargo transport. Increasing urbanization, economic growth, and tourism have led to a rise in both short-haul and long-haul flights, boosting fuel consumption for fixed-wing aircraft.

Despite this, conventional fuels continue to dominate due to their availability and lower costs. Fluctuating oil prices and geopolitical factors further impact fuel pricing, influencing airline operating costs. Additionally, advancements in fuel-efficient technologies and lightweight aircraft designs are shaping fuel consumption patterns in the fixed-wing aircraft sector.

Market Characteristics

The aircraft aviation fuel market is characterized by its dependence on fossil-based jet fuels like Jet-A and Jet-A1, which dominate due to their high energy density and established global supply chains. The market is driven by the growing demand for air travel, both for passenger and cargo transport, as well as military aviation. Fluctuating crude oil prices heavily influence fuel costs, impacting airline profitability and operational strategies.

The market is also seeing increasing pressure from environmental regulations aimed at reducing carbon emissions, prompting the development and gradual adoption of sustainable aviation fuels (SAF). While SAF remains a smaller segment due to higher costs and limited production, its role is expanding with government incentives and airline commitments to sustainability. Technological advancements in fuel-efficient aircraft and engines are helping to reduce overall fuel consumption, but the market remains largely reliant on conventional aviation fuels for the foreseeable future.

Global Aviation Fuel Market Report- Scope (Customizable)

| Scope | Description |

| Historic Period | 2018-2023 |

| Base Year (Esti.) | 2024 |

| Forecast Period (F) | 2025-2032 |

| Market Revenue | USD Million |

| Market by Fuel Type | Conventional Fuel and Sustainable Fuel |

| Market by Aircraft Type | Fixed Wing Aircrafts, Rotary Wings, and Unmanned Aerial Vehicle (UAV) |

| Market by Region | North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

| Countries Covered | U.S., Canada, Mexico; Germany, UK, Italy, France, Spain; China, India, Japan, South Korea, Malaysia, Singapore, Thailand, Vietnam, Australia & New Zealand; Brazil, Argentina; Saudi Arabia, United Arab Emirates (UAE), South Africa |

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?