Automotive Metal Stamping Market Overview

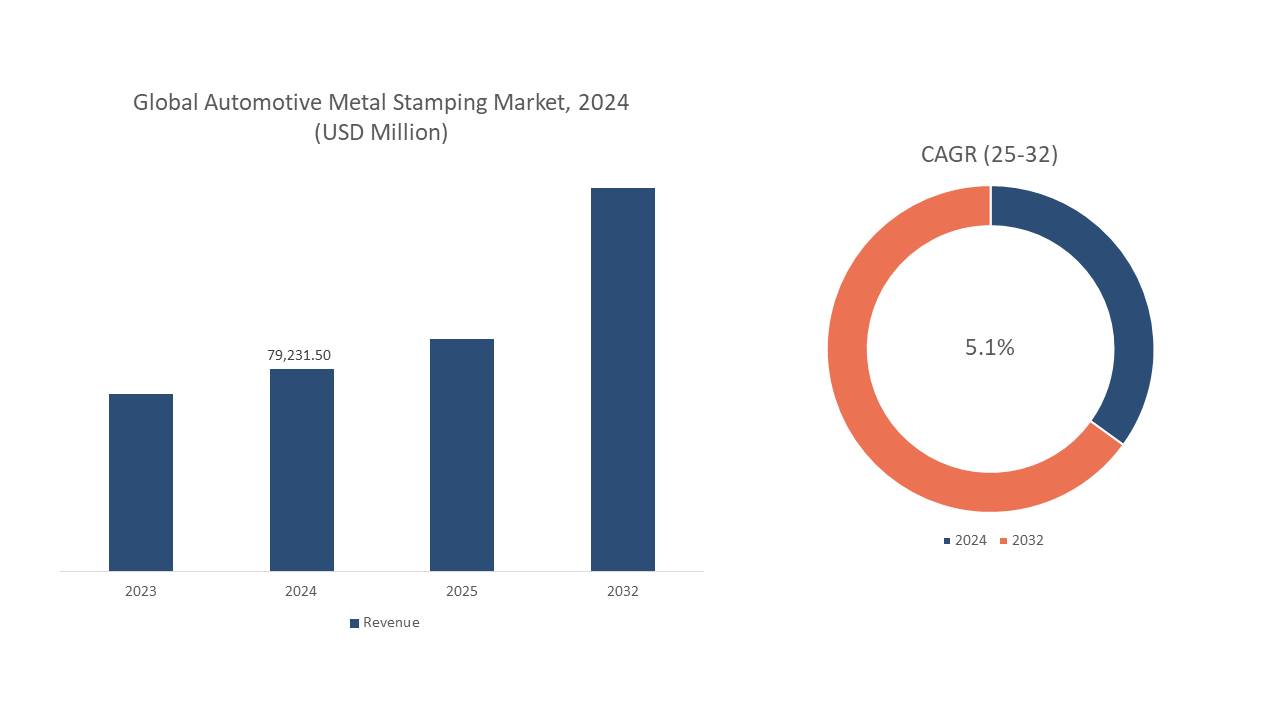

According to Novatrends Market Intelligence, the global automotive metal stamping market is valued at USD 79,231.50 million in 2024.The global automotive metal stamping market is experiencing robust growth, driven by increasing demand for vehicles, trend towards lightweight materials in car manufacturing to improve fuel efficiency, and metal stamping technology, such as the use of CNC machines, allow for faster, more precise production of complex parts.

Furthermore, the growing popularity of electric vehicles (EVs) creates a niche demand for metal stamping. While EVs may have fewer engine components, they require new components for battery enclosures and lightweight chassis design, areas where metal stamping is well-positioned.

Automotive Metal Stamping Market Recent Developments

The automotive metal stamping market is anticipated to propel at a compounded annual growth rate (CAGR) of 5.1% from 2024-2032. The automotive metal stamping market is witnessing significant expansion, driven by rising demand for electric vehicles from growing population especially across emerging economies such as China, India, and others.

The automotive metal stamping market is highly competitive due to the presence of major market players actively engaged in implementing strategic initiatives such as increasing investments, production expansion, enlarging distribution networks, and others. For instance,

- In June 2024, Martinrea International Inc. a prominent player across designing, development, production of lightweight structures, and propulsion systems for automotive industry announced an investment of USD 35.0 million to expand their Ridgetown plant to add a new stamping press, namely, SIMPAC. This introduction of new equipment is anticipated to assist the production of larger and more complex automotive components.

- In March 2024, Toyota Boshoku Tennessee, LLC (TBTN), announced an investment of USD 54.4 million for the expansion of their manufacturing operations as metal stamping facility in Jackson. This expansion is anticipated to support the company’s initiatives to cater customers through its subsidiary’s across the nation.

Regional Overview

Asia Pacific dominated the global automotive metal stamping market in 2024 with a market revenue share of above 45.7%. The regional dominance is acquainted by it’s powerhouse combination of long-standing car manufacturing centers and fast-growing economies.

China, India, Japan, and South Korea are dominating countries across the market, generating high demand for stamped metal parts. The increasing popularity of electric vehicles in these countries further accelerates the market's expansion.

China's dominance in electric vehicles further strengthens the region's position. According to the International Energy Agency (IEA) reports China holds nearly half of all electric vehicles globally, and in 2024, exported 35% of the world's electric vehicles.

Recognizing this trend, regional players are ramping up production capacity for metal stamping. For instance, Chinese company Tenral announced capacity expansion plans of their metal stamping operations in March 2024 to meet the growing demand for EV components.

U.S. Automotive Metal Stamping Market Overview

After a period of fluctuation, the U.S. auto industry is experiencing a period of growth. Rising disposable incomes and a growing population, particularly in developing regions, translate to a higher demand for new cars and trucks. This translates directly to a need for more stamped metal components for bodies, frames, and other vehicle parts.

A major trend in the U.S. auto industry is the focus on fuel efficiency, to achieve this, car manufacturers are increasingly using lightweight materials such as aluminum and high-strength steel. Metal stamping is perfectly suited for shaping these materials due to its ability to create complex parts with high precision and consistency.

Furthermore, advancements in automation and computer-controlled machines (CNC) are revolutionizing the production process. These technologies enable faster, more precise, and more cost-effective production of complex metal parts. This translates to benefits for both automakers and metal stamping companies, ultimately leading to a more efficient and competitive auto industry.

Technology Overview

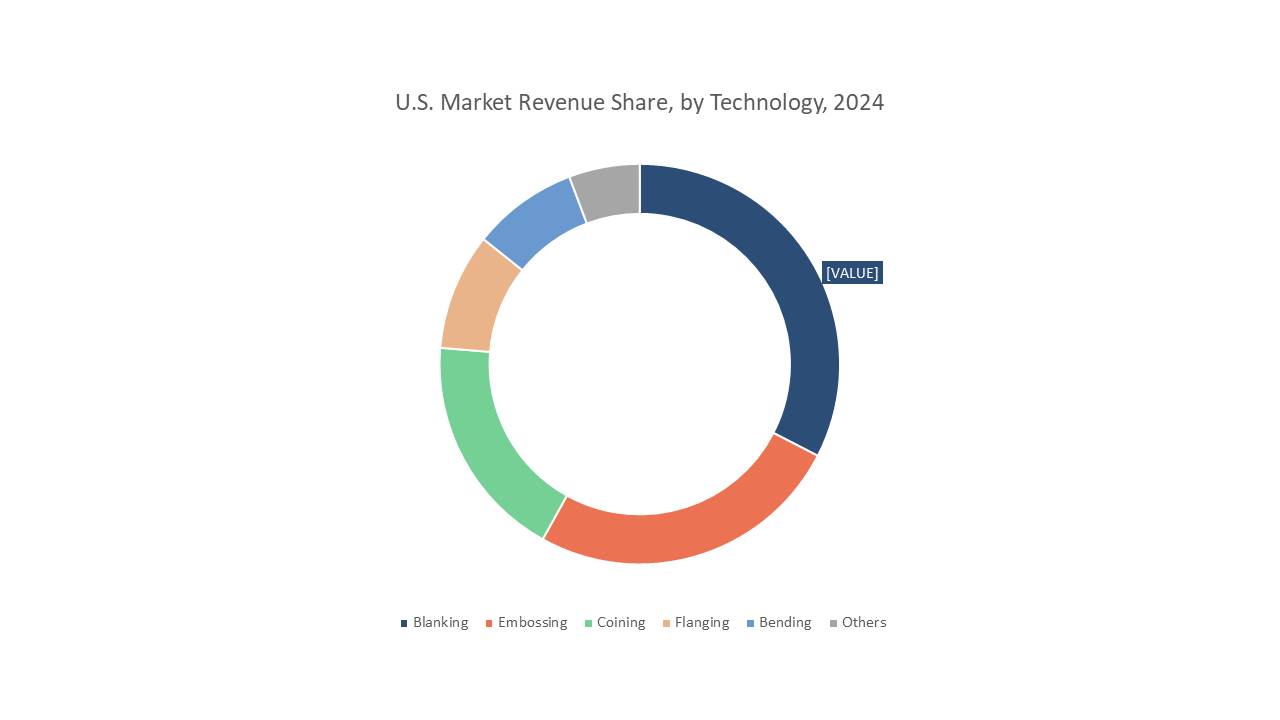

Blanking dominated the technology segmentation across the global automotive metal stamping market in 2024 with a market revenue share of 32.6%. Blanking, the process of shearing sheet metal into desired shapes, is the foundation of automotive metal stamping. For a successful blanking operation, achieving clean cuts with minimal distortion and defects is crucial.

Modern car designs often feature intricate body panels, brackets, and other components with complex shapes. Blanking excels at creating these parts with high accuracy and repeatability. The sharp shearing action of the punch and die allows for clean cuts along defined edges, even for intricate geometries. This capability is crucial for achieving the sleek aesthetics and functionality demanded in today's vehicles.

The metal stamping market is witnessing a surge in partnerships between metal stampers and original equipment manufacturers (OEMs), especially across the blanking process. This collaboration allows for closer integration and development of innovative solutions. For instance, in February 2024, Fischer Group in partnership with TRUMPF implemented the groundbreaking TruLaser 8000 Coil Edition blanking system at their headquarters. This fully automated system processes massive quantities of coiled sheet metal, revolutionizing production with superior material utilization and resource efficiency.

Process Overview

Roll forming dominated the scrap type segmentation across the global market space in 2024 with a market revenue share of 32.7%. Roll forming, a continuous process for shaping sheet metal into desired cross-sections, is carving a niche in the automotive metal stamping market. The automotive industry's relentless pursuit of fuel efficiency necessitates lightweight materials. Roll forming excels at shaping high-strength steel and aluminum, materials prized for their strength-to-weight ratio. This allows for the creation of lightweight yet robust structural components for vehicles.

Hot stamping, a process that combines heat treatment with metal forming, is revolutionizing the automotive metal stamping market by enabling the creation of exceptionally strong and lightweight car parts. Hot stamping utilizes high-strength steel alloys that are heated to a specific temperature before being formed into parts. This process creates components with exceptional strength-to-weight ratios. This allows car manufacturers to reduce vehicle weight without compromising passenger safety or structural integrity, a critical factor for improved fuel efficiency.

Vehicle Type Overview

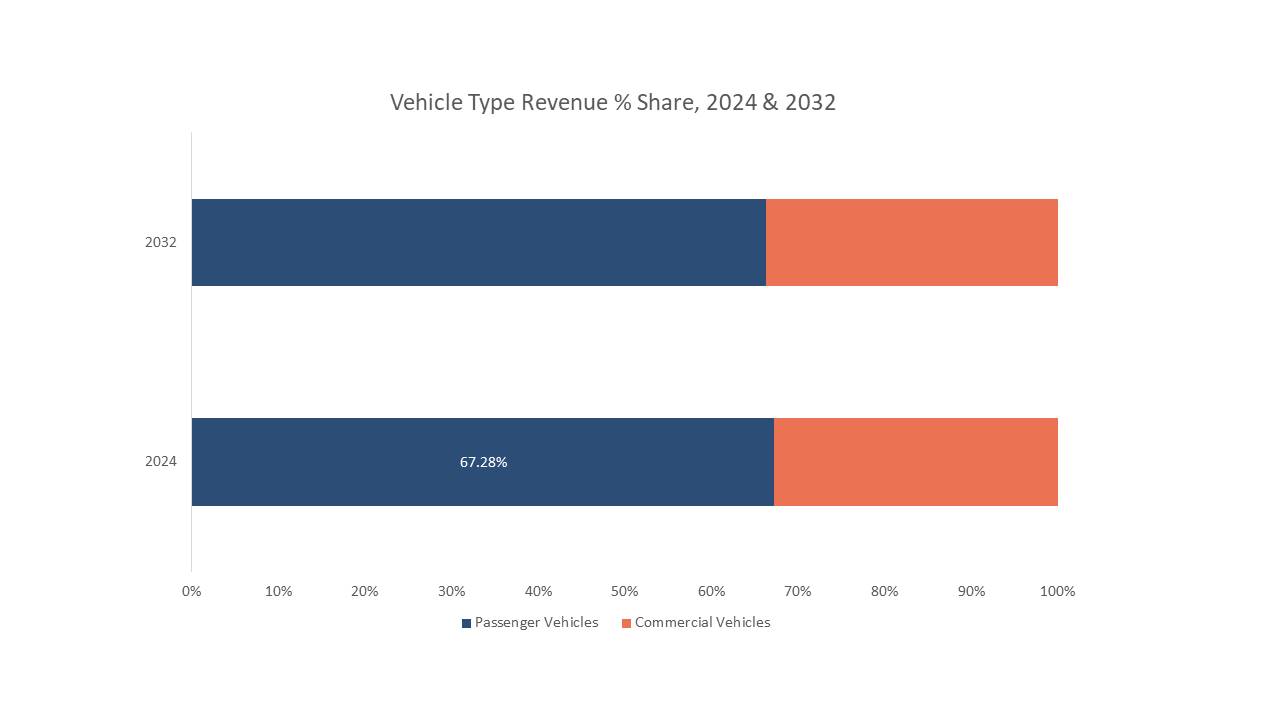

Passenger vehicles dominated the vehicle type segmentation across the global market space in 2024 with a market revenue share of 67.2%. The global passenger vehicle market is experiencing steady growth, particularly in developing economies with expanding middle classes and increasing disposable incomes. This translates to a need for more cars, directly impacting the demand for metal stamped components like body panels, chassis parts, and structural elements.

The global fleet of passenger vehicles is aging, leading to a growing demand for replacement parts. Metal stamping plays a vital role in producing these replacement components, ensuring a steady demand stream beyond new vehicle production.

Governments around the world are implementing stricter fuel economy regulations to combat climate change. This pushes automakers towards lightweight vehicle designs to improve fuel efficiency. Metal stamping excels at working with lightweight materials like aluminum and high-strength steel, allowing car manufacturers to meet these regulations without sacrificing vehicle performance.

Market Characteristics

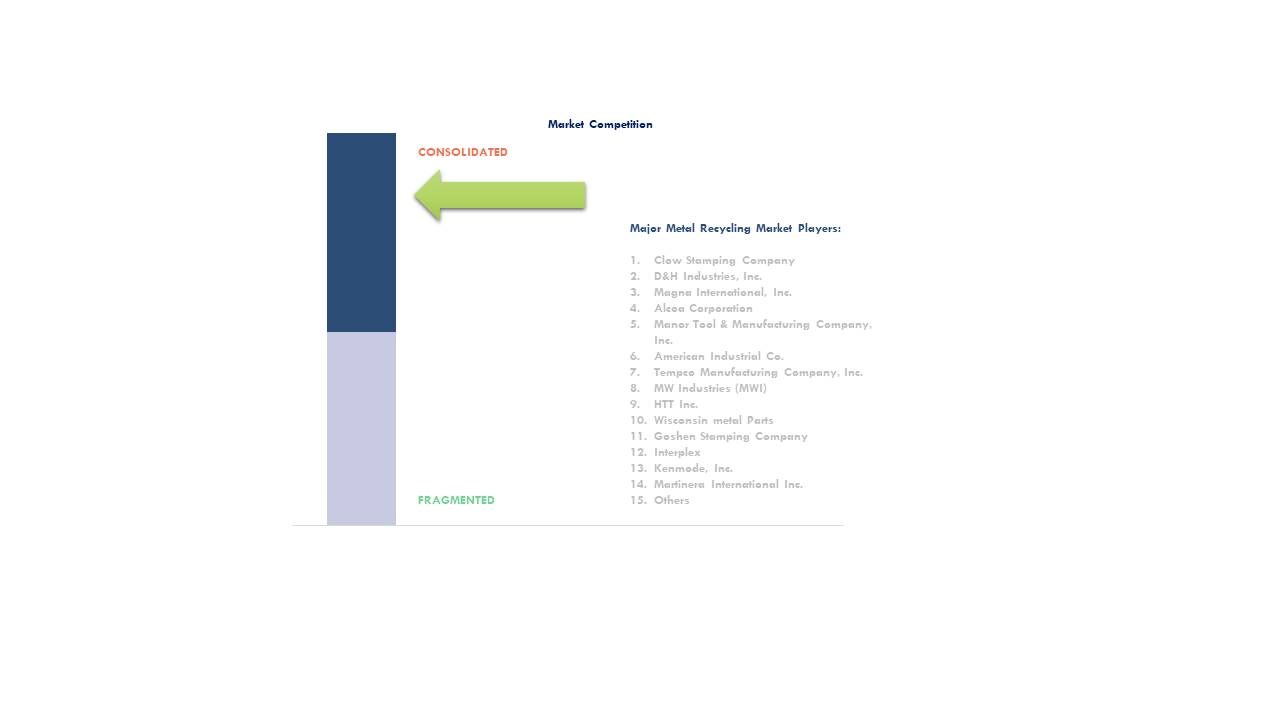

The automotive metal stamping market is becoming increasingly competitive with a mix of established players and new entrants vying for the market share. Vendors in the market are adopting strategies such as new product developments, mergers & acquisitions, and others.

The automotive metal stamping market is a dynamic and competitive landscape populated by a diverse range of players. Large multinational companies possess vast production capacities, advanced technologies, and established relationships with major automakers. Several regional players hold significant market share within their respective territories.

These companies often specialize in catering to the specific needs of regional automakers and may possess expertise in working with local materials or regulations. These companies include Mahindra CIE Automotive (India) and China Die Casting Technology Group Co. (China).

Various companies act as suppliers to original equipment manufacturers (OEMs) and Tier 1 automotive suppliers. They focus on high-volume production of specific stamped metal parts according to customer specifications. Contract stampers compete on factors like cost-efficiency, agility, and responsiveness to customer demands.

Global Automotive Metal Stamping Market Report- Scope (Customizable)

|

Scope |

Description |

|

Historic Period |

2018-2023 |

|

Base Year (Esti.) |

2024 |

|

Forecast Period (F) |

2025-2032 |

|

Market Revenue |

USD Million |

|

Market by Technology |

Blanking, Embossing, Coining, Flanging, Bending, and Others |

|

Market by Process |

Roll Forming, Hot Stamping, Cold Stamping, Sheet Metal Forming, Metal Fabrication, and Others |

|

Market by Vehicle Type |

Passenger Vehicles and Commercial Vehicles |

|

Regions Covered |

North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

|

Countries Covered |

U.S., Canada, Mexico; Germany, UK, Italy, France, Spain, Russia; China, India, Japan, South Korea, Malaysia, Singapore, Thailand, Vietnam, Australi & New Zealand; Brazil, Argentina; Saudi Arabia, United Arab Emirates (UAE), Iran, South Africa |

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?