Market Overview

According to Novatrends Market Intelligence, the Global Aircraft Flight Control System Market was valued at USD 18.6 billion in 2025 and is anticipated to propel at a growth rate of 7.4% from 2026-2036.

The global aircraft flight control system market encompasses the hardware and software systems enabling pilot control of aircraft attitude, speed, and trajectory across commercial aircraft control, military aircraft flight control, UAV flight control, drone flight control, and emerging eVTOL flight control platforms. Fly-by-wire system technology — replacing mechanical cable linkages with electronic flight control computer command-and-response architecture — is now standard across all new commercial aircraft and advanced military platforms. Flight control computer processors, flight control actuator electro-hydraulic and electromechanical systems, and flight control software represent the core component segments. Flight management system, autopilot system, and automatic flight control capabilities are increasingly integrated into unified avionics architectures. Aircraft safety systems including envelope protection, stall prevention, and aircraft automation through auto-throttle and autoland are central to modern digital flight control. Aerospace control systems for UAV flight control and drone flight control are growing rapidly with military and commercial unmanned aircraft adoption, while eVTOL flight control for urban air mobility vehicles represents a significant emerging market requiring new flight control software and aircraft actuation system architectures.

Market Dynamics

The market is driven by commercial aviation fleet expansion requiring advanced fly-by-wire system and flight control computer fitment in new single-aisle and widebody aircraft, military modernization programs upgrading military aircraft flight control to digital flight control with enhanced aircraft safety systems, and rapid UAV flight control and drone flight control market growth from defense and commercial unmanned system deployments. Aerospace aftermarket demand for flight control actuator overhaul, flight management system upgrades, and autopilot system software updates on in-service fleets generates significant recurring revenue. eVTOL flight control certification activity is accelerating with FAA and EASA approval of urban air mobility platforms from Joby, Archer, and Lilium. In January 2024, Collins Aerospace expanded flight control computer and aircraft actuation system production for Boeing and Airbus narrow-body programs, while Honeywell Aerospace launched new autopilot system and automatic flight control software for regional and business aviation aircraft avionics upgrades. Aircraft OEM backlogs at Boeing and Airbus and growing aerospace aftermarket demand are sustaining strong flight control software and digital flight control equipment demand through 2036.

Segment Analysis

By System Type: Primary Flight Controls holds the largest share of the Aircraft Flight Control System market, supported by strong adoption and well-established supply chains across key end-use industries. Secondary Flight Controls is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Technology: Fly-by-Wire holds the largest share of the Aircraft Flight Control System market, supported by strong adoption and well-established supply chains across key end-use industries. Mechanical is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Platform: Commercial Aircraft holds the largest share of the Aircraft Flight Control System market, supported by strong adoption and well-established supply chains across key end-use industries. Military Aircraft is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

By Component: Flight Control Computer holds the largest share of the Aircraft Flight Control System market, supported by strong adoption and well-established supply chains across key end-use industries. Flight Control Actuator is the fastest-growing segment, propelled by rising investments and expanding application scope in high-growth sectors.

Recent Developments in Aircraft Flight Control System Market

- In January 2024, Collins Aerospace expanded flight control computer and aircraft actuation system production for Boeing 737 MAX and Airbus A320 family fly-by-wire system commercial aircraft control supply, advancing digital flight control capabilities and aircraft safety systems for global commercial aircraft OEM demand.

- In April 2024, Honeywell Aerospace launched next-generation autopilot system and automatic flight control software for business aviation and regional aircraft, integrating flight management system with AI-driven aircraft automation and advanced aircraft avionics architecture for digital flight control upgrades.

- In July 2024, Moog Inc. expanded flight control actuator and aircraft actuation system manufacturing for military aircraft flight control in F-35 and Eurofighter programs, advancing electromechanical flight control actuator technology for UAV flight control and eVTOL flight control platforms as part of a broader aerospace control systems expansion.

- In September 2024, Safran Electronics & Defense introduced flight control computer and flight control software for next-generation commercial aircraft control and military aircraft flight control, incorporating enhanced aircraft safety systems with envelope protection and automatic flight control modes for Airbus and Dassault programs.

- In December 2024, BAE Systems expanded UAV flight control and drone flight control systems for military unmanned platforms, launching new aerospace control systems with AI-assisted aircraft automation and redundant fly-by-wire system architecture for Group 3-5 unmanned aircraft safety systems certification.

- In March 2025, Joby Aviation certified eVTOL flight control and aircraft actuation system architecture with FAA for its eVTOL air taxi, demonstrating advanced flight control software, automatic flight control, and aircraft safety systems meeting Part 23 airworthiness standards for urban air mobility commercial aircraft control operations.

Top Aircraft Flight Control System Market - Key Market Players

- Collins Aerospace (RTX)

- Honeywell Aerospace

- Moog Inc.

- Safran Electronics & Defense

- BAE Systems

- Joby Aviation

- Woodward Inc.

- Parker Hannifin (Aerospace)

- Liebherr Aerospace

- GE Aviation Systems

- Thales Avionics

- Curtiss-Wright Corporation

- Kearfott Corporation

- Elbit Systems

- L3Harris Technologies

Global Aircraft Flight Control System Market Report- Scope (Customizable)

Scope | Description |

Historic Period | 2021-2024 |

Base Year (Esti.) | 2025 |

Forecast Period (F) | 2026-2036 |

Market Values | USD Billion |

By System Type | Primary Flight Controls, Secondary Flight Controls, High Lift Systems |

By Technology | Fly-by-Wire, Mechanical, Hydraulic |

By Platform | Commercial Aircraft, Military Aircraft, UAV, eVTOL |

By Component | Flight Control Computer, Flight Control Actuator, Sensors |

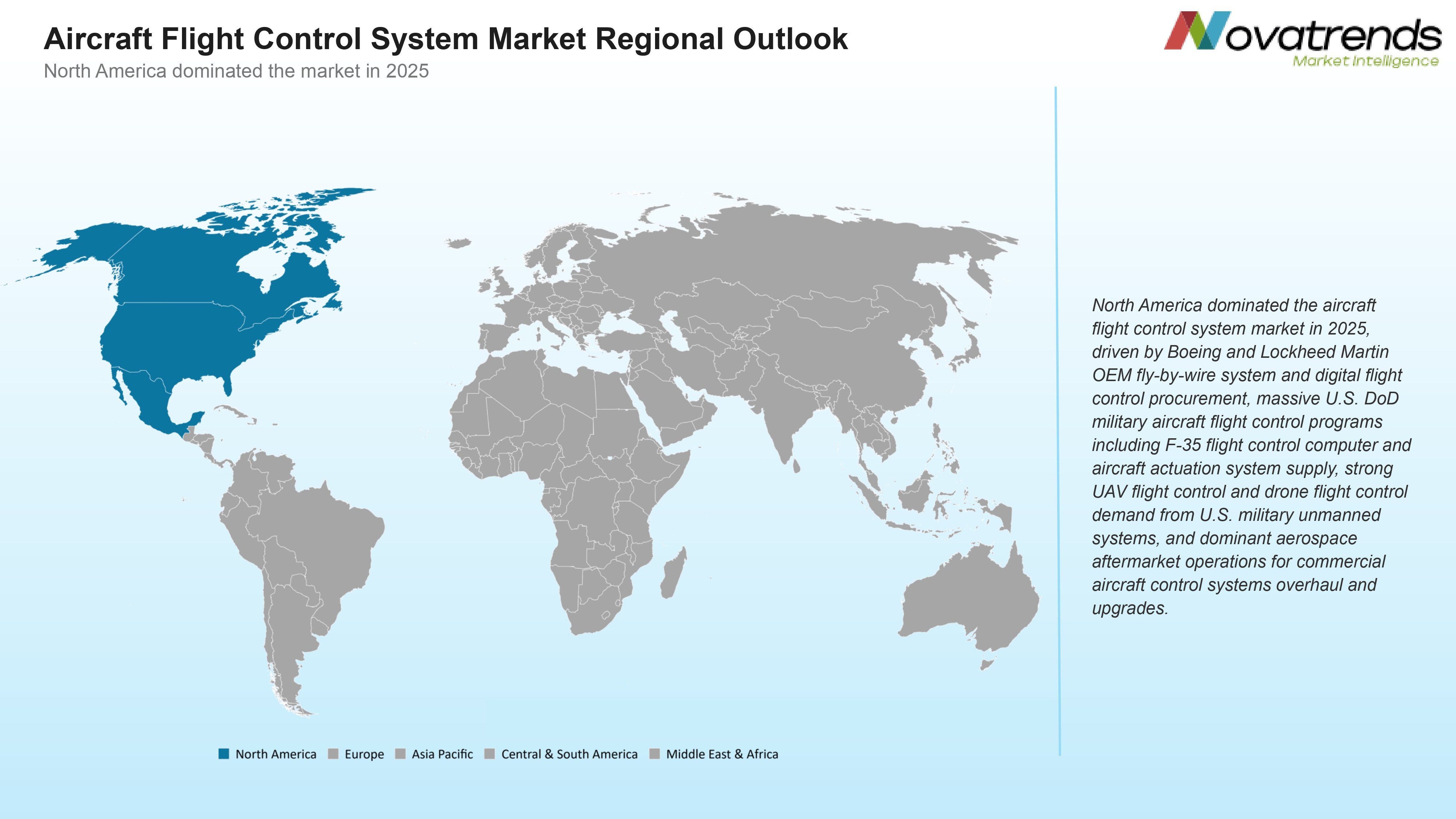

Market by Region | North America (NA), Europe (EUR), Asia Pacific (APAC), Central & South America (CSA), and Middle East & Africa (MEA) |

Countries Covered | U.S., Canada, and Mexico; Germany, France, UK, Russia, Italy, Spain, and Netherlands; China, India, Japan, South Korea, and Australia; Brazil, Argentina; Saudi Arabia, UAE, Turkey, Egypt, and South Africa |

Detailed Market Segmentation

- By System Type (Revenue in USD Million)

- Primary Flight Controls

- Secondary Flight Controls

- High Lift Systems

- By Technology (Revenue in USD Million)

- Fly-by-Wire

- Mechanical

- Hydraulic

- By Platform (Revenue in USD Million)

- Commercial Aircraft

- Military Aircraft

- UAV

- eVTOL

- By Component (Revenue in USD Million)

- Flight Control Computer

- Flight Control Actuator

- Sensors

- By Region (Revenue in USD Million)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Russia

- Italy

- Spain

- Netherlands

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Central & South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- Egypt

- South Africa

- North America

GET A FREE SAMPLE

GET A FREE SAMPLE

Need a custom report?

Need a custom report?